🔬Reporting Season... err, Report!

Plus: Nvidia CEO is having a better week than me; and much more!

"The four most expensive words in the English language are, 'This time it’s different'"

- Sir John Templeton

“Money and women are the most sought after and the least known about of any two things we have”

- Will Rogers

Solid turnaround day for the big US markets with the S&P 500 +1.6% and Nasdaq +2.6%. Small-Cap still found a way to work with the Russell 2000 +0.5%.

7 of 11 sectors closed higher led by a rebounding Tech (+4.0%) following some decent reporting (see below). Defensive Health Care (-0.4%) was worst, giving back some of its recent winnings.

Japan raised it’s central bank policy rate 0.25% from 0-0.1%. Marks the highest level since 2008. The BOJ also announced plans to halve bond-buying program over the next two years.

Fed meeting was a bit of a nothing burger. Positive rhetoric shift aligning with September rate cut, such as focusing on dual mandate (inflation and maximum employment) instead of just talking about inflation the whole damn time.

Notable companies:

Microsoft (MSFT) [-1.1%]: Mixed fiscal Q4 results, guided Q1 below; AI demand commentary upbeat, expects Azure growth to accelerate in 2H FY25 as AI capacity constraints lessen.

Advanced Micro Devices (AMD) [+4.4%]: Q2 EPS and revenue beat, GM ahead; guided Q3 revenue midpoint ahead, increase in Data Center GPU to $4.5B from $4B; further enterprise server share gains with AI traction, some raising MI300 revenue growth forecasts through FY25.

Nvidia (NVDA) [+12.8%]: Positive read-throughs from Microsoft capex and AMD earnings; reassigned Top Pick rating at Morgan Stanley expecting concerns to fade over time.

ASML Holding (ASML) [+8.9%]: New US rule on foreign chip equipment exports to China will exempt key allies, including the Netherlands and South Korea.

Way more below in ‘Market Movers’

Street Stories

Reporting Season Report

As of July 30th, 199 companies in the S&P 500 have reported earnings, and with the market looking super f***** jittery for a direction, this is probably the most important, make-or-break earnings season we’ve seen in a while.

Right off the bat, the market has been quite supportive of earnings so far: The average company has seen their shares trade +0.4% in the trading day following their earnings release, and roughly 58% of companies have managed to trade higher.

Also worth noting is that there haven’t been too many blow-ups either. So far only 3 companies have traded down by more than 20% following earnings (Dexcom, Lamb Weston and Edwards Lifesciences). Not too shabby!

On the actual reporting front, it’s been pretty much par for the course. 36% of companies have posted revenue beats compared to Wall Street estimates, which is roughly 2x as many as have posted misses.

8% of companies have posted significant beats of >5%, while only 4% of companies standout as having had significant misses.

On the Earnings Per Share front, things are looking even better: 63% of companies have beat Street estimates with a whopping 23% of them being >10% above forecast.

I think it’s fair to say that there are no significant red flags here.

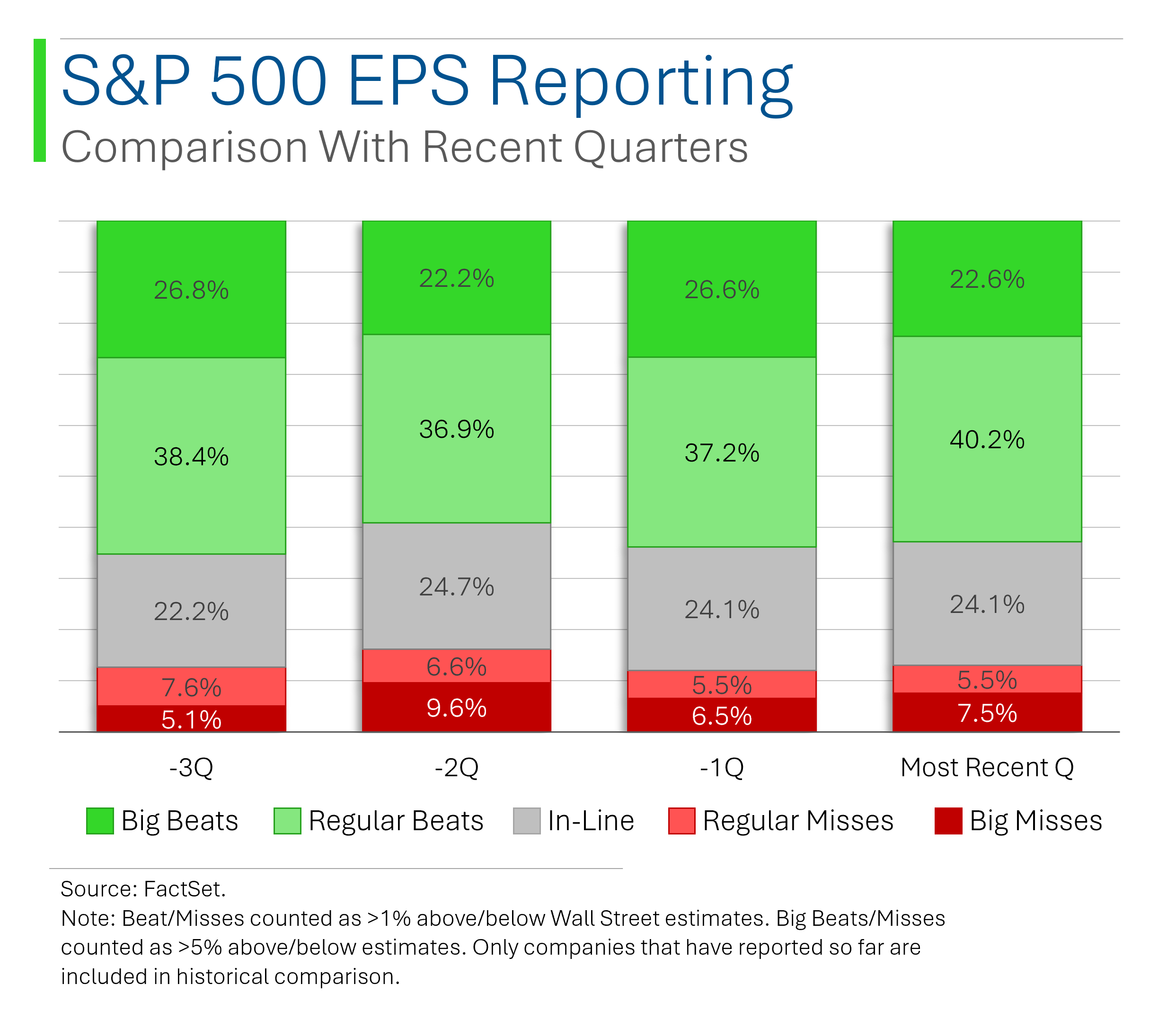

And looking at recent history, quarterly revenue results seem to be a bit weaker than we’ve seen in recent quarters but nothing too dramatic. For example, 35.7% of companies have posted revenue beats this quarter, which compares to a 40.8% average over the last three quarters.

Not great, but not terrible.

That said, on the EPS front things are pretty bang-on with history: 62.8% of companies posted beats vs. a last three quarter average of 62.7%.

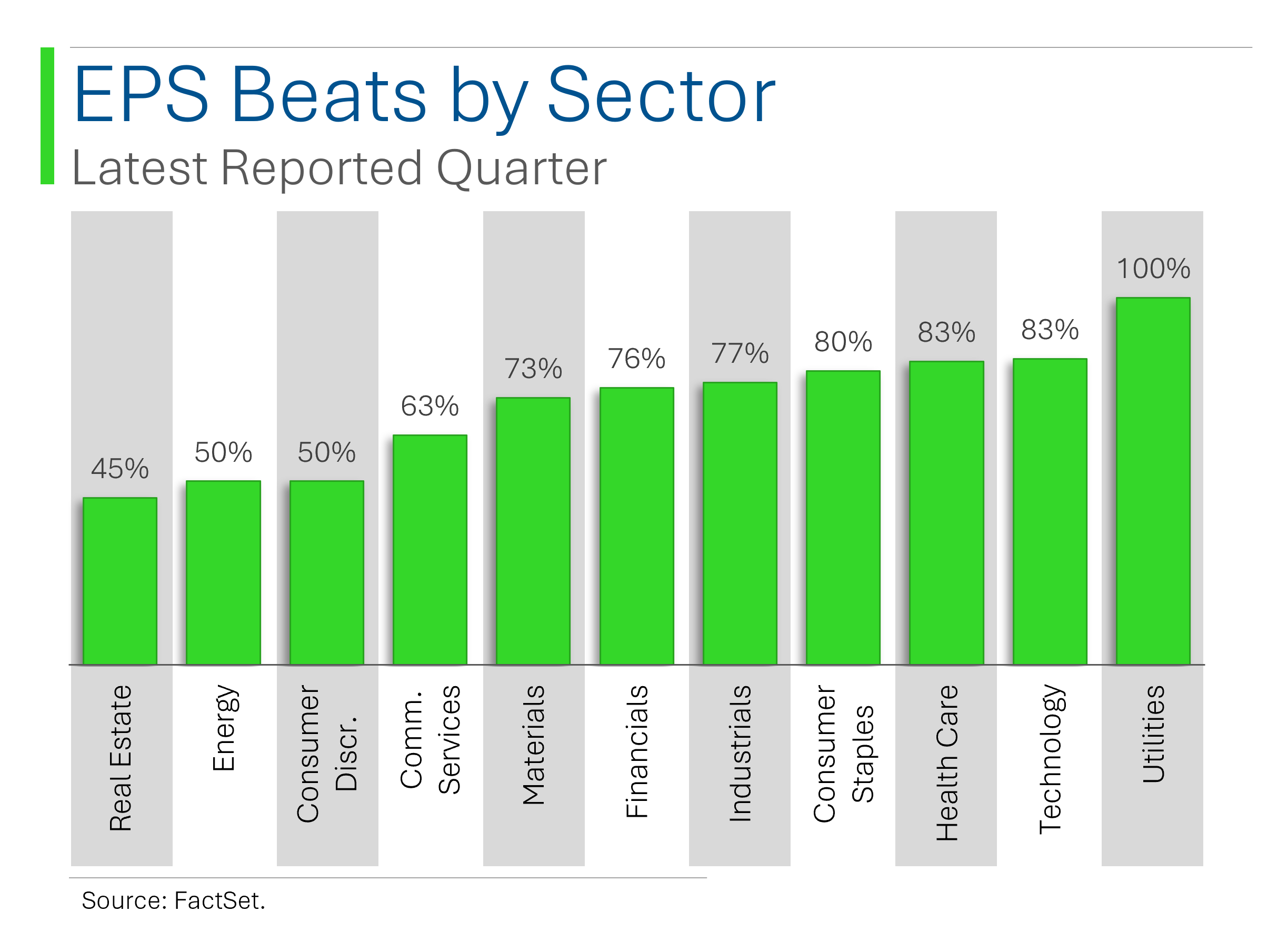

Lastly, I wanted to tie things into sectors a bit. See, not all sectors were created equally, and there are a lot of different drivers at play across industries.

For example, while most of the recent Tech sell-off can be attributed to high valuations and the big year-to-date rally in the shares, the fact that only 33% of Tech companies have posted revenue beats this quarter is also an important consideration. After big rallies and mega hype, the expectation bar gets raised higher and higher, and if your stock is up 90% this year, your shares aren’t gunna get a pass just for posting an in-line quarter.

Also interesting is that industrials - the biggest beneficiary of the recent rally - have only seen 26% of its companies post revenue beats. Not exactly generating a lot of investor love here…

Things look a bit better for Tech and Industrials when looking at EPS, but if you’re looking at ‘growth' companies I’d argue that revenue matters a wee bit more than earnings - not least of which because it’s a lot easier to play accounting games the lower you get down an income statement.

To wrap this up, this earnings season is super important to maintain investor confidence that companies are still able to show strength. I don’t think this will go down in anyone’s books as a particularly great season but thus far there aren’t any sinister trends emerging.

It remains to be seen how the remaining 60% of companies will show, and more importantly how they will be received by an increasingly picky set of investors.

Average $11.4 Billion Day

Microsoft reported its Q4 yesterday (weird year end, eh) which was kinda lame and sent the shares down -1.1%. I’ve talked a lot about Microsoft lately so I won’t get into it.

However, they did say some nice stuff about AI demand and Nvidia - which really needs a friend right now - and that was enough to propel the shares up +12.8%. I’ve also talked a lot Nvidia lately so I won’t get into it.

What I will mention is that with 863 million shares that means Co-Founder and CEO Jensen Huang saw his net worth jump by $11.4 billion in just one day. Sure, his $101 billion net worth might not be back to its June 18th peak of $127 billion, but he’s definitely having a better week than me (my basement flooded and my fridge broke).

If you missed it, I did a pretty nifty deep-dive on Nvidia and Microsoft a few weeks back:

Joke Of The Day

Stockbroker: What is a million years like to you?

God: Like one second.

Stockbroker: What is a million dollars like to you?

God: Like one penny.

Stockbroker: Can I have a penny?

God: Just a second…

Hot Headlines

Yahoo Finance / The world’s greatest investor, Nancy Pelosi, bought Nvidia shares Friday and dumped Microsoft. You can’t make this stuff up.

CNBC / Bill Ackman’s Pershing Square withdraws IPO as demand for offering waned. I’m sure the final straw was me making fun of him yesterday about downsizing from $25 billion to $2 billion. Haters move markets.

CBS / Amazon is legally responsible for recalling dangerous products sold on its site. The U.S. Consumer Product Safety Commission issued a decision against Amazon, determining the retailer was a "distributor" of products that are defective or fail to meet federal safety standards, including faulty carbon monoxide detectors, hairdryers without electrocution protection and flammable kid’s pajamas. I’m sure a few ppl at Temu had a stroke after this.

Hot Hardware / Ford files alarming patent that rats out speeding drivers to police. Titled "Systems and Methods for Detecting Speeding Violations," the patent describes how one's car can be used to detect if nearby vehicles were being driven above the posted speed limit. Thought they were running out of ways to make Ford less cool, and then boom!

CNBC / AI-powered financial advisor has quickly gained $20 billion in assets. The automated financial advisor, called PortfolioPilot, has added 22k users in the two years it’s been around. Hints at large disruption coming for the investment advice business. I, for one, welcome our new machine overlords.

Trivia

This week’s trivia is on Investing 101.

In finance, liquidity refers to:

A) The ease of converting assets to cash

B) The amount of liquid in a company's water cooler

C) The duration of investment assets

D) The change in net operating cash flow of a businessThe Capital Asset Pricing Model (CAPM) is used to:

A) Determine yield on a bond or annuity

B) Calculate expected return on an investment based on its risk

C) Price capital goods

D) Model the capital of a city

'Systemic Risk' refers to:

A) The risk that computer and technology failures pose to financial markets

B) The risk of collapse of an company, market or financial system

C) The risk associated with a particular operating system

D) The undiversifiable investment risk associated with the market

(answers at bottom)

Market Movers

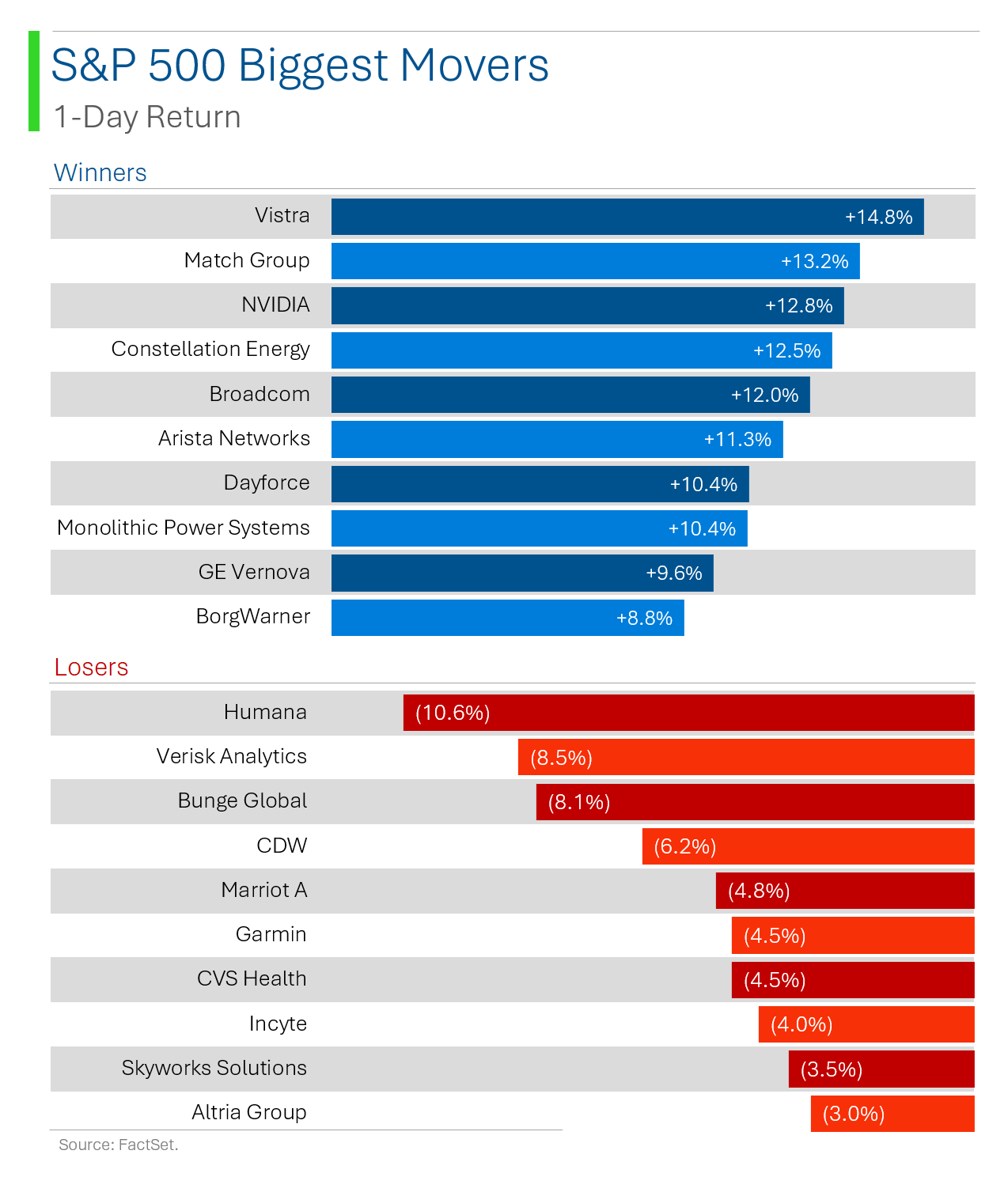

Winners!

Match Group (MTCH) [+13.2%]: Q2 earnings, revenue, and OM better; paying users and revenue per payer ahead; stabilization in MAU trends and improving payer trajectory; Q3 guidance below and cut FY revenue-growth guide on exit from live-streaming services; report better than feared.

NVIDIA (NVDA) [+12.8%]: Positive read-throughs from Microsoft capex and AMD earnings; reassigned Top Pick rating at Morgan Stanley expecting concerns to fade over time.

ASML Holding (ASML) [+8.9%]: New US rule on foreign chip equipment exports to China will exempt key allies, including the Netherlands and South Korea.

BorgWarner (BWA) [+8.7%]: Q2 revenue light but EBIT and EPS ahead; lowered high end of FY sales guidance but boosted margin outlook and low end of EPS range; positive takeaways on margins, execution; 2H buyback acceleration, ePropulsion restructuring.

Caesars Entertainment (CZR) [+8.3%]: Q2 earnings beat though revenue missed; driven by cost controls with expenses declining; strong trends in Las Vegas and Caesars Digital; construction disruptions impacted regional performance, notably in New Orleans.

Advanced Micro Devices (AMD) [+4.4%]: Q2 EPS and revenue beat, GM ahead; guided Q3 revenue midpoint ahead, increase in Data Center GPU to $4.5B from $4B; further enterprise server share gains with AI traction, some raising MI300 revenue growth forecasts through FY25.

DuPont de Nemours (DD) [+4.1%]: Q2 earnings and revenue beat; strength in Electronics & Industrial driven by semi demand recovery and higher OLED volumes; Water & Protection decline narrower than feared; raised FY guidance ranges.

Kraft Heinz (KHC) [+4%]: Q2 EPS beat but revenue missed; reaffirmed FY24 EPS guidance, cut organic net sales forecast citing cautious consumer sentiment; positive on efficiency improvements and easing revenue headwinds, Foodservice segment opportunities.

T-Mobile US (TMUS) [+3.9%]: Q2 revenue beat with core adjusted EBITDA in line; FCF ahead; Wireless customer adds a bright spot; postpaid ARPU topping consensus; trimmed FY EBITDA midpoint but raised FCF and postpaid net adds guides.

Johnson Controls International (JCI) [+3.7%]: FQ3 EPS beat though revenue missed; lower NFC drove the beat; FQ4 EPS guidance beat, FY24 EPS guidance raised; targeting ~100% of FCF returned to shareholders; CEO succession search as George Oliver to retire.

MasterCard (MA) [+3.6%]: Q2 earnings and revenue beat; healthy consumer spending, robust cross-border volume growth, and solid demand for value-added services; raised FY net revenue guidance midpoint.

KKR (KKR) [+3%]: Q2 adj EPS beat, FRE EPS up 25% y/y; distributable earnings and FRE margin strong; FRE beat driven by higher transaction fees and FRPR with management fees in line.

Starbucks (SBUX) [+2.6%]: Fiscal Q3 sales light but EPS in line with help from cost controls; NA sales declined less than expected while international worse with China a big drag; progress on cost/margin and opportunities in operating/marketing initiatives; confirmed Elliott stake and constructive conversations.

First Solar (FSLR) [+2.4%]: Q2 EPS and revenue beat; FY24 guidance reiterated, low-end of range more likely; EPS upside driven by ASP and IRA credits; strong demand for utility solar driven by data centers; flagged political risks.

Automatic Data Processing (ADP) [+1.9%]: Fiscal Q4 revenue and EPS beat; FY guidance better at midpoints; acceleration in PEO growth, conservative ES growth guide, better margin expansion.

Losers!

Pinterest (PINS) [-14.5%]: Q2 earnings and revenue better; MAU ahead with ARPU in line; Q3 revenue guide below Street; cited tougher comps and FX pressures; broad ad strength in retail and tech but softness from food/beverage advertisers; flagged decline in ad pricing.

Humana (HUM) [-10.6%]: Q2 EPS and revenue beat; FY24 guidance reaffirmed; raised 2024 individual Medicare Advantage growth target by 75,000 members; warned of potential profit hit this year and next, pulled 2025 profit forecast due to disappointing government Medicare reimbursement rates.

Marriott International (MAR) [-4.8%]: Q2 EPS slightly ahead, revenue missed; Q3 EPS guidance missed; FY24 EPS lowered, RevPAR growth range narrowed due to weaker operating environment in Greater China and softer expectations in U.S. & Canada.

Lantheus Holdings (LNTH) [-4.5%]: Q2 EPS missed but revenue beat; FY24 EPS guidance lowered due to recent transactions; revenue guidance reaffirmed; Pylarify beat, growing 29.8% y/y.

Skyworks Solutions (SWKS) [-3.5%]: Fiscal Q3 results and guide largely in line; Apple contribution to revenue below normal seasonality; flagged lower iPhone 16 content; positive AI-driven refresh commentary.

Penumbra (PEN) [-3.4%]: Q2 EPS, EBITDA, and revenue ahead; cut FY24 revenue guidance citing weaker China macro and European product delays; weaker GM expansion expected in FY24 on expense timing; multiple downgrades due to guidance cuts, reduced business visibility.

Altria Group (MO) [-3.1%]: Q2 earnings and revenue missed; flagged lower net revenues in smokeable products due to lower shipment volumes and higher promotional investments; solid results in oral tobacco products with higher pricing and lower promos; narrowed FY EPS guidance range.

Microsoft (MSFT) [-1.1%]: Mixed fiscal Q4 results, guided Q1 below; focused on unexpected 1pp slowdown in Azure growth to 30%, at low end of 30-31% guidance; AI demand commentary upbeat, expects Azure growth to accelerate in 2HFY25 as AI capacity constraints lessen.

Market Update

Trivia Answers

A) Liquidity is the ease of converting assets to cash.

B) CAPM calculates expected return on an investment based on its risk (using Beta as the risk input).

B) Systemic Risk is the risk of collapse of a company, market or financial system. If you picked D, that’s ‘systematic risk’. Muahaha.

Thank you for reading StreetSmarts. We’re just starting out so it would be great if you could share StreetSmarts with a friend that might be interested.

Great read! Thanks for the report!