🔬The Waning Rate Hype: an Explainer, Apple Announces New Policy To Gouge Developers, and Much More

"The stock market is filled with individuals who know the price of everything, but the value of nothing"

- Jesse Livermore

“I think it's wrong that only one company makes the game Monopoly”

- Steven Wright

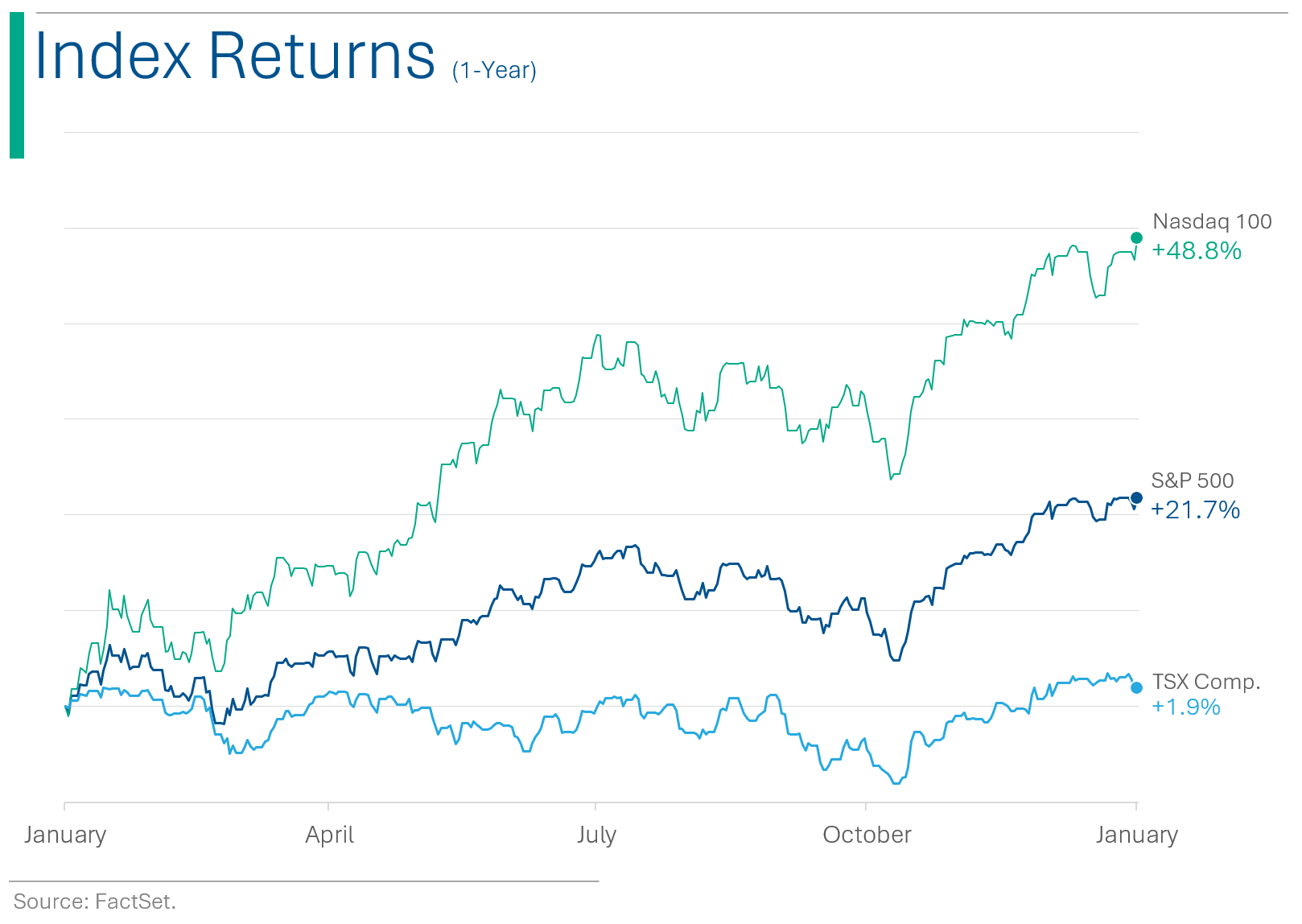

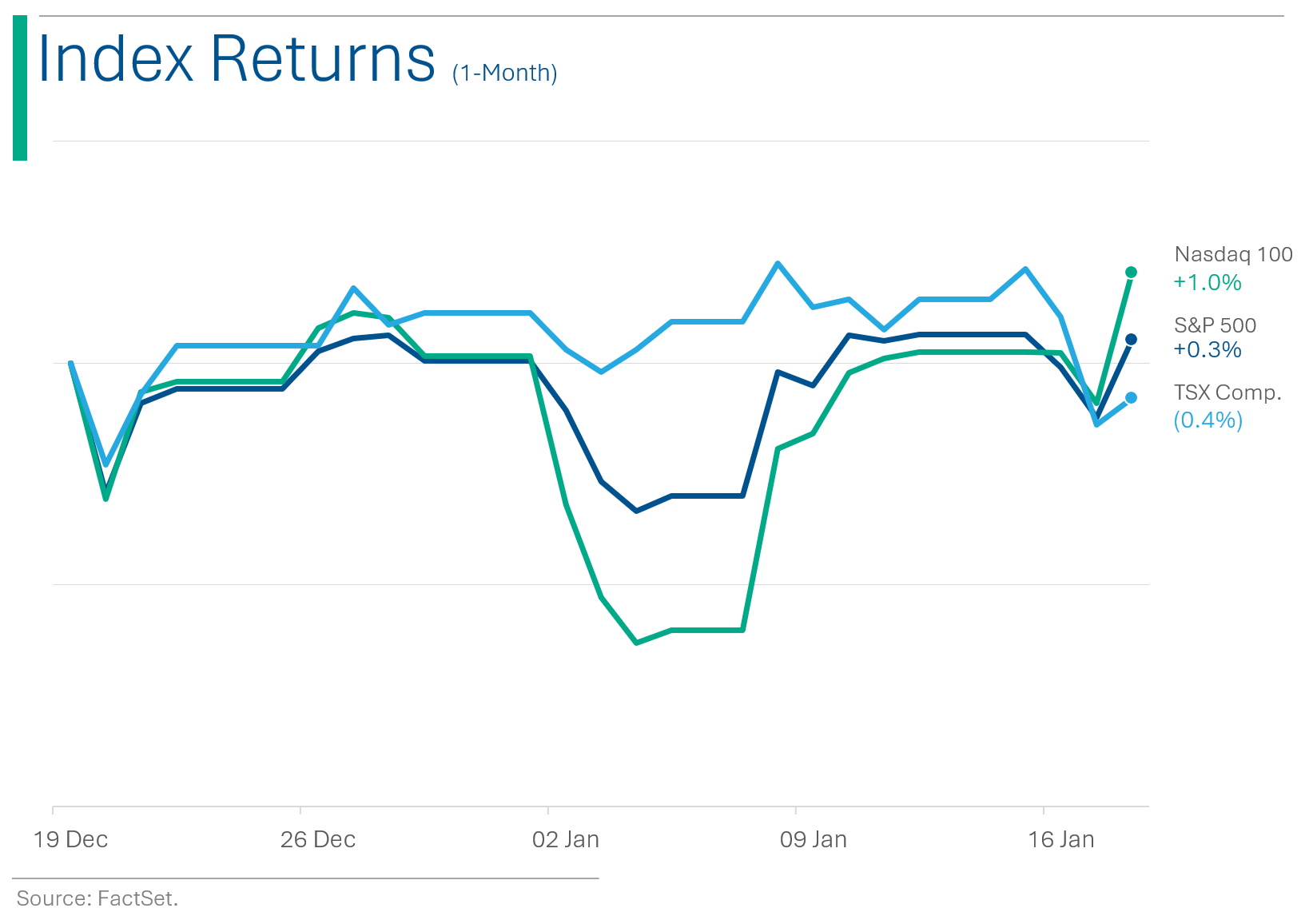

Solid day for the big markets with the S&P 500 +0.88% and Nasdaq +1.35%.

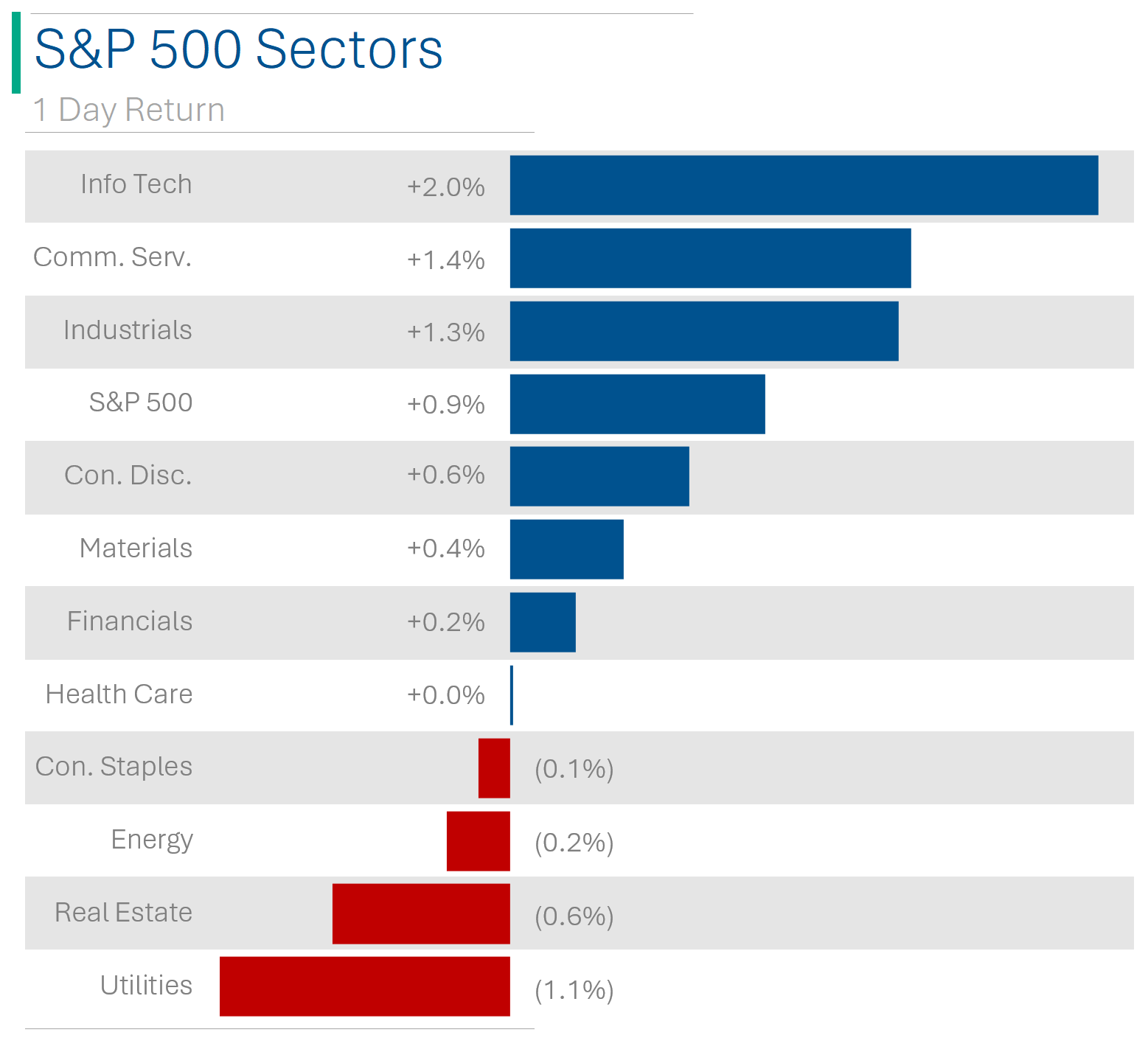

7 of 11 sectors closed in the green, with Info Tech (2.0%) and pseudo-tech Communication Services (+1.4%). While ‘safe’ Utilities (-1.1%) wet the bed again.

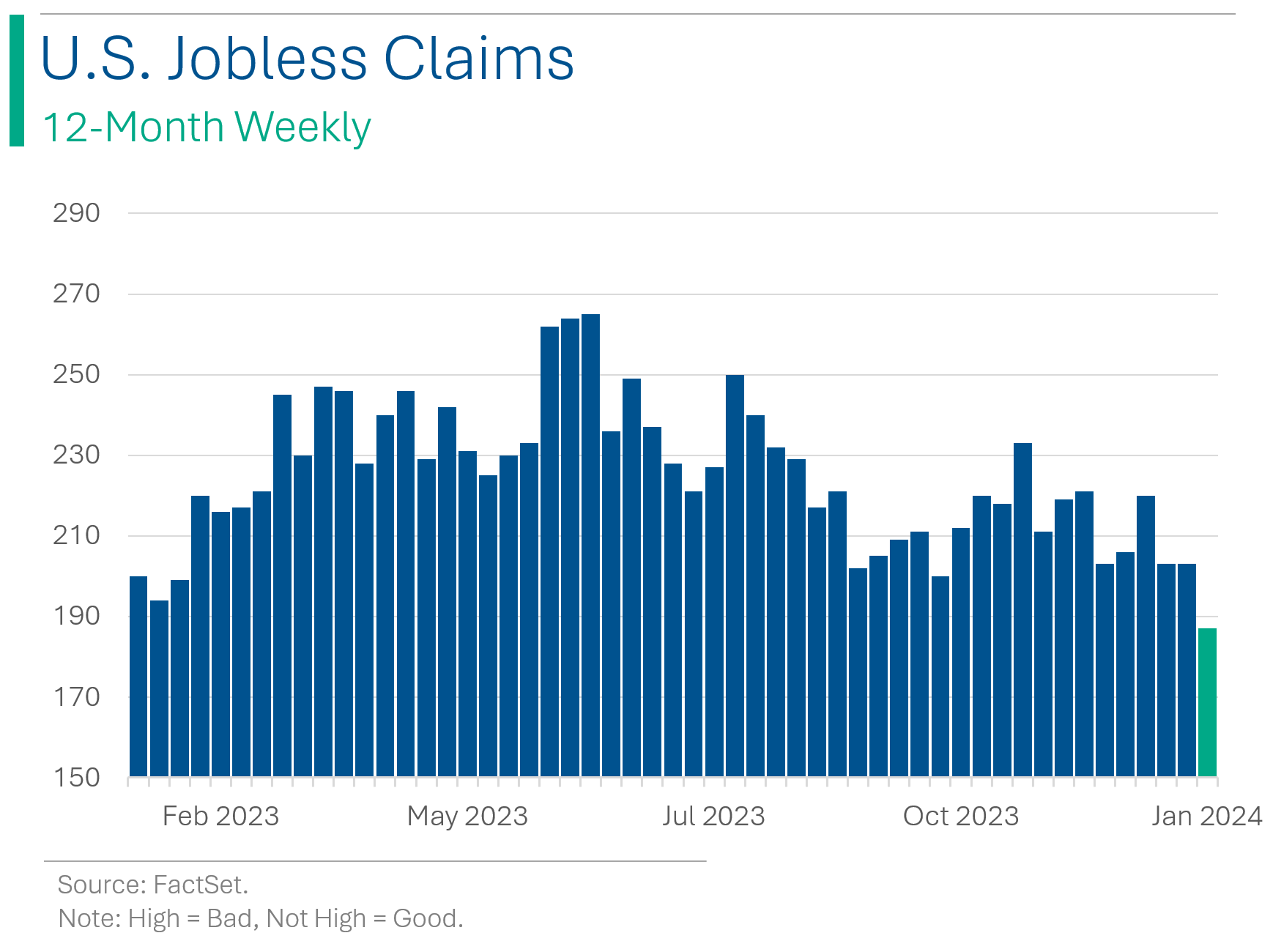

Oil popped +2.0% (Red Sea stuff) while US jobless claims came in super low at 187k vs. 203k last week, 2023 average of 224k.

The world’s largest chip maker Taiwan Semiconductor was up 9.8% after posting strong Q4 results. IE: They added $47 billion in market cap - or NT$1.6 trillion if you prefer. Damn.

Street Stories

Rate Hype Wanes

When markets went on a tear at the end of 2023 the catalyst was heavily linked to Inflation and the Fed. Specifically that, with inflation coming down after a stubborn summer/autumn, the Fed looked increasingly like it had the greenlight to start cutting rates (which stocks like).

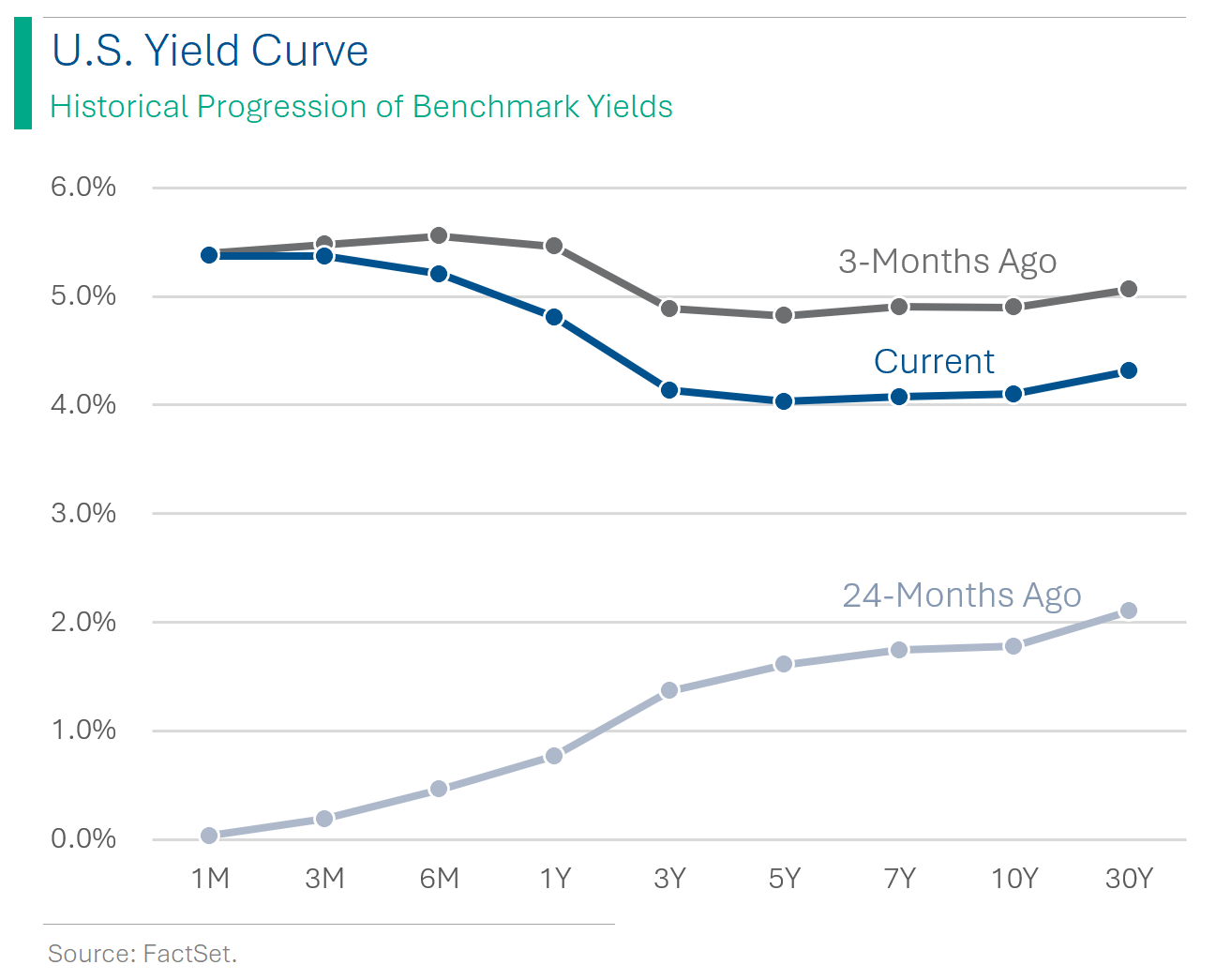

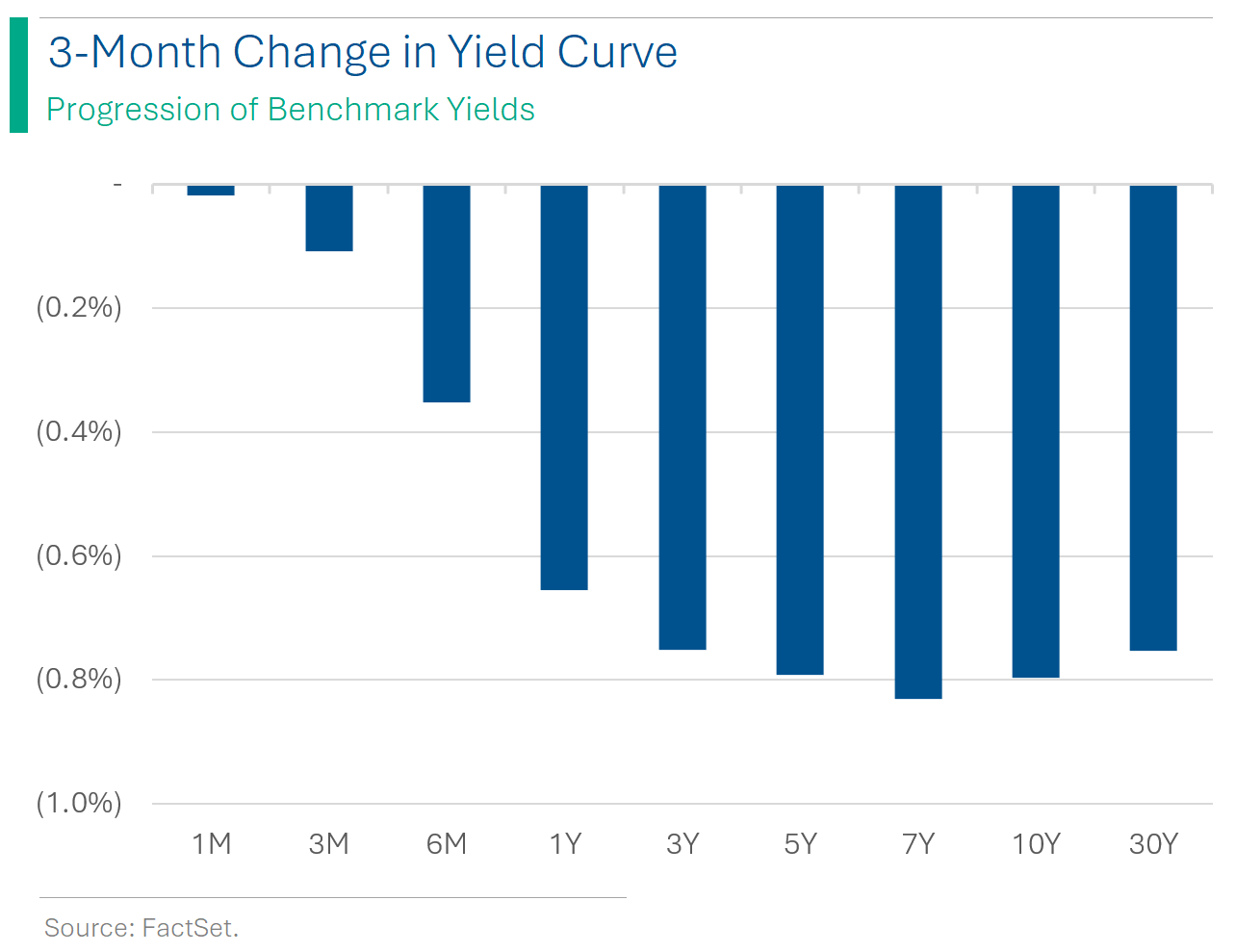

Beyond the ~+16% run the S&P 500 had from the end of October until year’s end, we saw pretty massive moves in the US Yield Curve, as expectations turned towards a US Fed that would be free to start slashing rates.

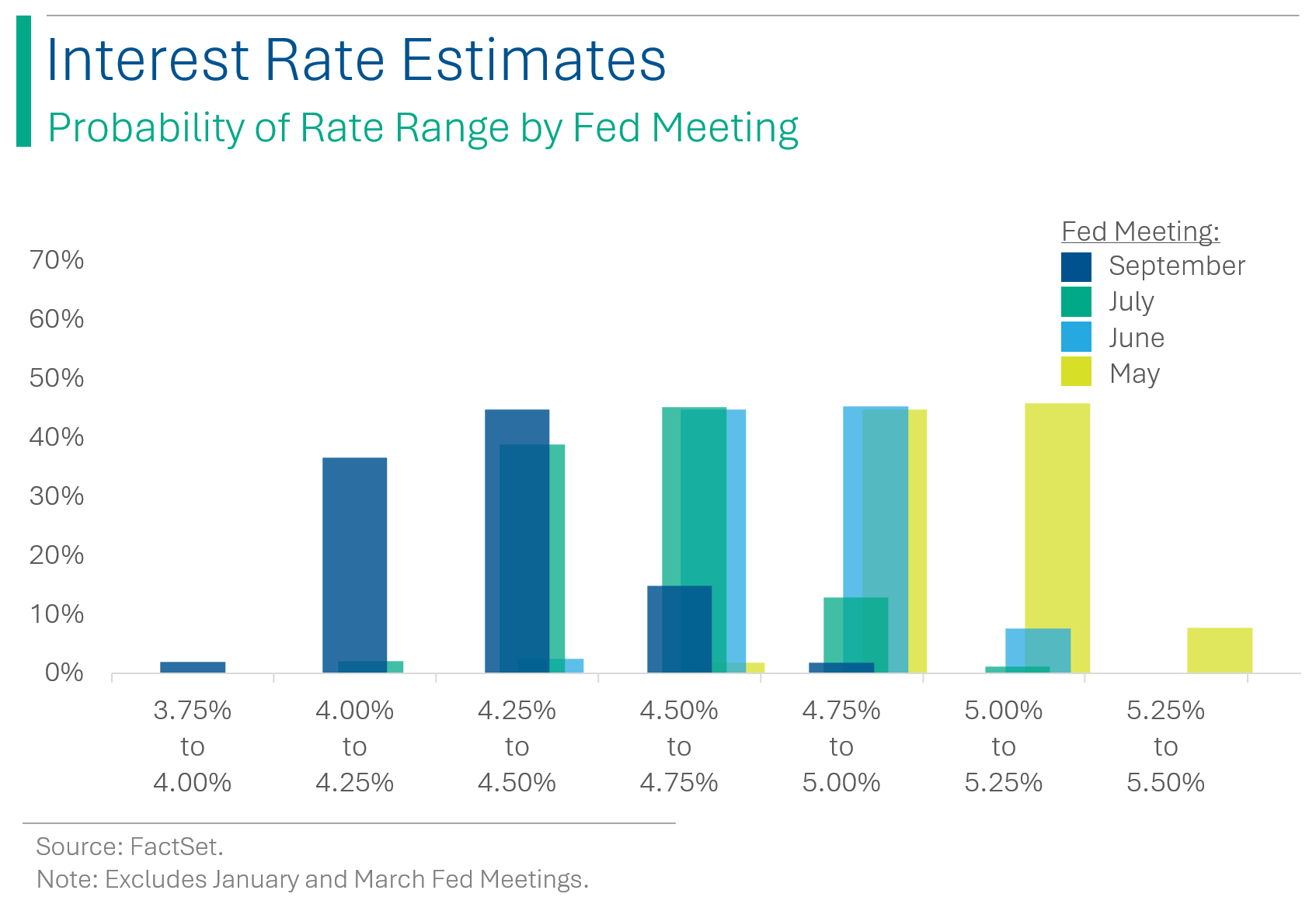

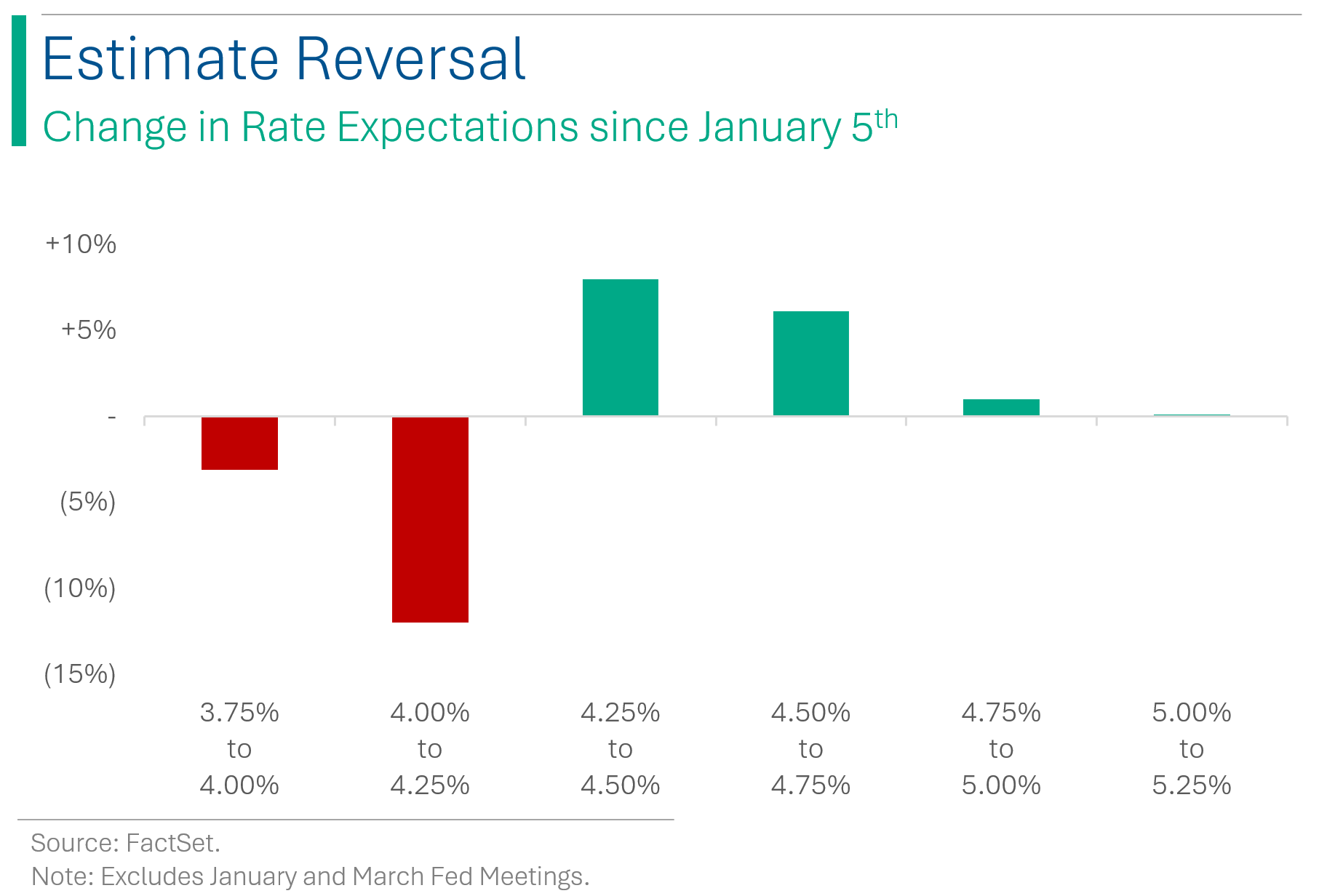

The Fed’s ‘Dot Plot’ - it’s sorta guidance on where committee members see interest rates heading - implied around 0.75% of interest rate cuts in 2024. The markets, however, had grander ambitions and priced in around 1.5% of cuts this year. Bit of a disconnect.

And that leads us to today, where a bit of an about-face is taking place. While recent ‘Fedspeak’ - rhetoric by Fed officials where they hint at policy positions - hasn’t exactly been ‘hawkish’, they have moved more towards the position of ‘what’s the rush?’

Whereas rate cuts were seen as essential to help stave off recession, recent economic data out of the US has been quite strong: Q3 GDP came in at 5.2%, the labour market appears relatively healthy, and ancillaries like consumer spending and housing starts have all been pretty positive. To the Fed, why risk cutting too early and risk inflation going back up (super embarrassing) when there doesn’t appear to be any rush?

The result is that the market is starting to cool it with these aggressive forecasts, and expectations have actually moved backwards to pricing in fewer 2023 cuts. For example, the probability of the Fed’s target range being 4.00% to 4.25% following their September meeting have gone from 49% to 37%, while the 4.25% to 4.50% bucket is now the dominant expectation (ie: down 1%) .

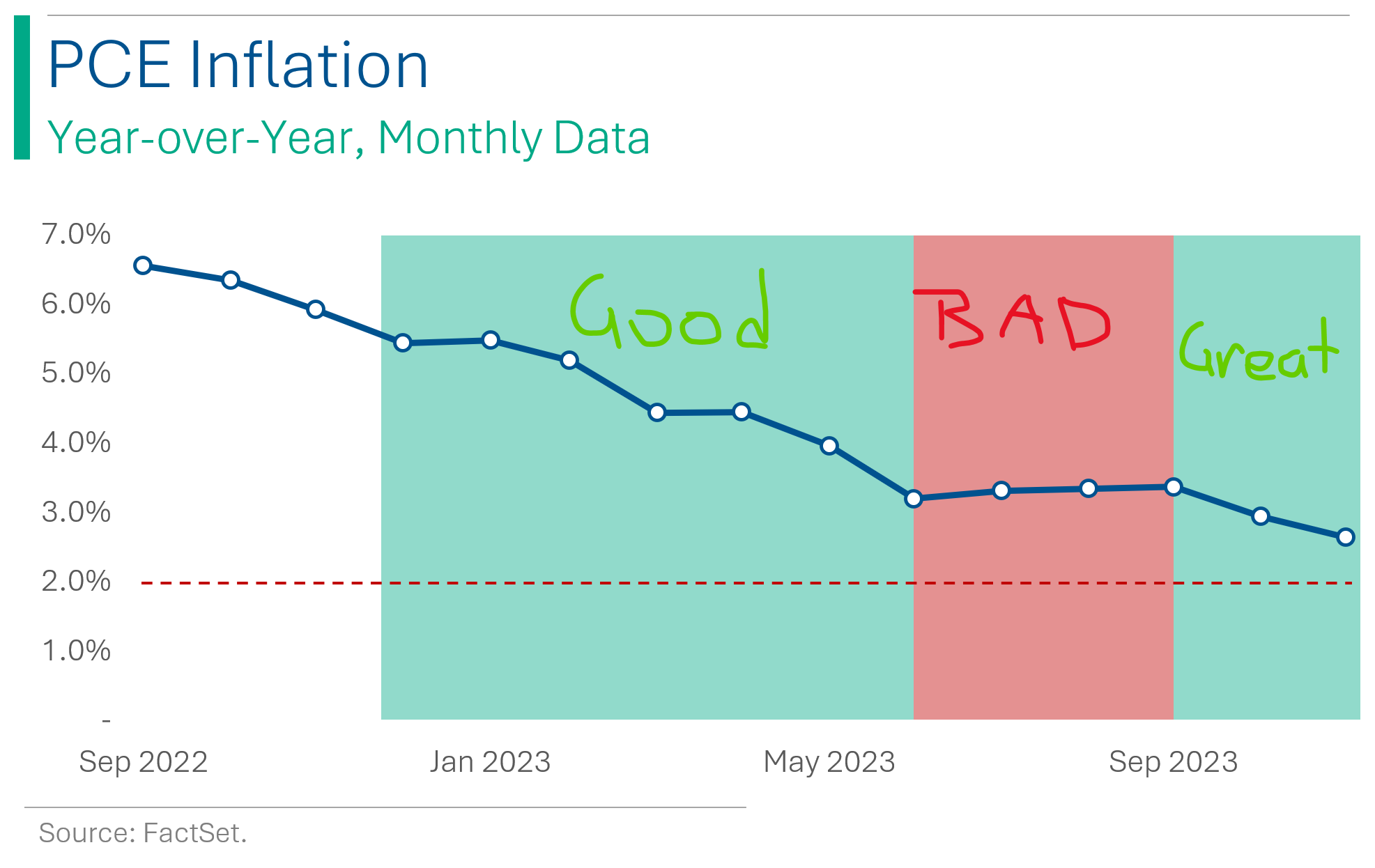

Time will tell where things end up settling. December Personal Consumption Expenditures (PCE) - the Fed’s preferred measure of inflation - will be released on January 26th and the next Fed meeting will take place January 30th to 31st. The results of which will likely go a long way towards reconciling the disconnect between what the Fed is planning and what the market is pricing in.

Apple's 27% Solution: Creative Compliance and the Art of Walking the Antitrust Tightrope

In a bold move that might remind some of a plot twist in Succession, Apple has implemented new App Store policies, mandating a 27% commission for developers using alternative payment methods, a response akin to sticking to the letter but not the spirit of a U.S. Supreme Court decision and international legal challenges.

The genesis of this saga dates back to Apple's legal scuffle with Epic Games, where Apple was partially reprimanded but emerged largely unscathed, except for a requirement to allow developers to guide customers to external payment methods (instead of the 30% App Store change). Unsurprisingly, developers and industry observers have raised their eyebrows at Apple's interpretation of 'compliance', accusing it of undermining the court's intention to foster greater competition and choice.

Meanwhile, Apple, seemingly unphased, continues to navigate a sea of global legal challenges and investigations, including the European Union’s Digital Markets Act, with the grace of a tech giant walking a tightrope over regulatory waters. Amidst all this, Apple's financial might, bolstered by billions from the App Store, remains as robust as ever, even as iPhone sales show signs of cooling - perhaps proving that in the tech world, drama and profits can coexist rather comfortably.

Where’s the Vol?

The market’s favourite volatility measure, the VIX, bottomed out in December to its lowest level since before the pandemic. Lately, though, it has been on the move and is just a titch below the 15-level that is often pointed to as the end of market complacency. And while it’s not at an alarming point (its 20-year average is 19.3), the market seems increasingly primed to make some large moves (direction TBD).

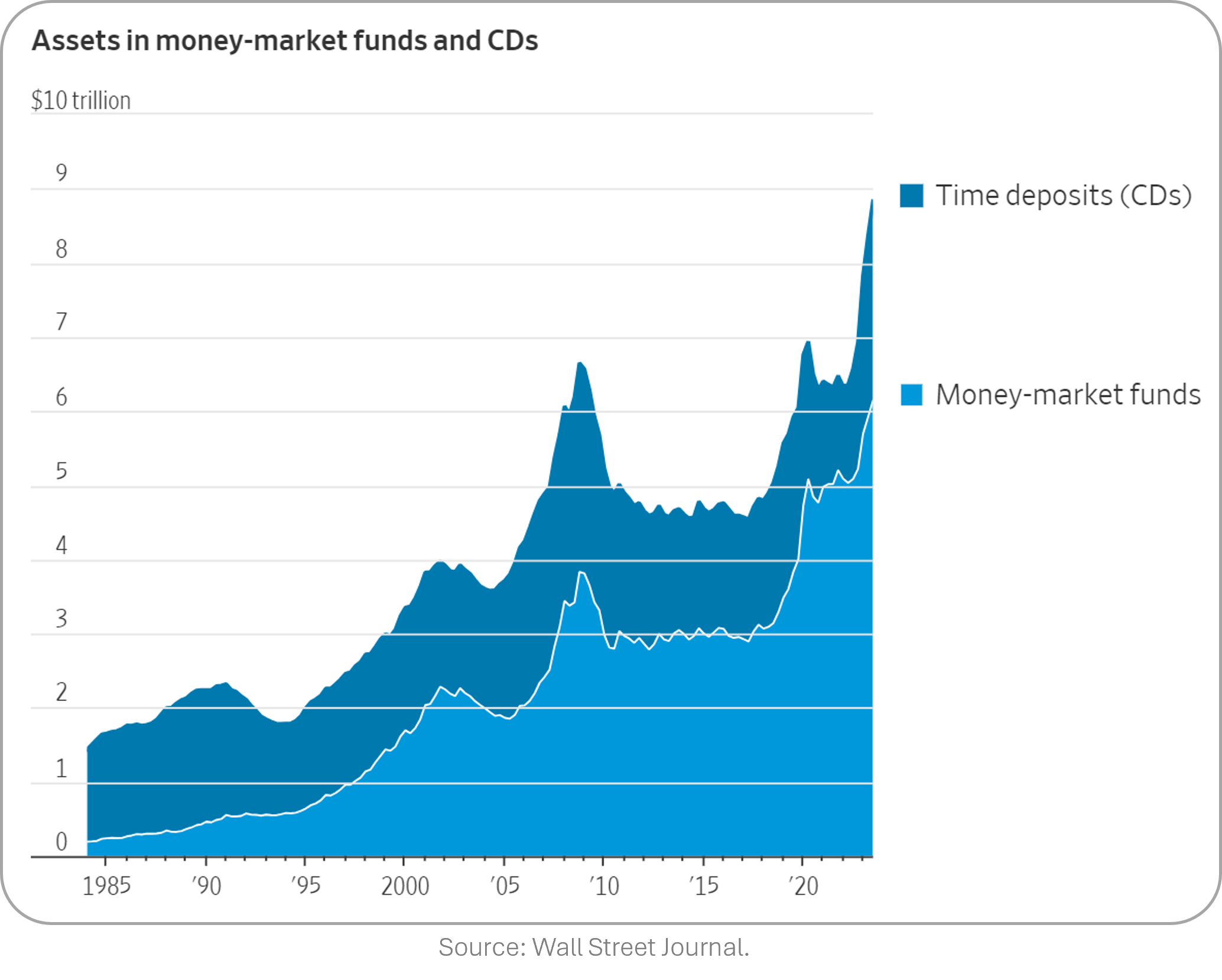

Wall Street's $8.8 Trillion Waiting Game

Wall Street is eyeing the over $8.8 trillion in low-risk money-market funds and CDs, anticipating that falling interest rates might redirect this substantial capital towards stocks and bonds. Historically, money-market funds have maintained high asset levels even when rates drop. However, given the scale of current rates, significant substitution is expected. The direction of these substantial funds is closely tied to the trajectory of interest rates, which are expected to decrease more smoothly compared to past rapid rate cuts. (WSJ has more on this cash pile)

Jobless Claims Hit Snooze, Economy Wakes Up Energized

U.S. unemployment claims unexpectedly fell to 187,000 in the week ending January 13, the lowest level in over a year, indicating a resilient labor market. The decrease, led by a significant drop in New York, continued a trend of low layoffs, although economists caution against reading too much into these volatile weekly figures. While other reports suggest some moderation, the robust job market and a rise in building permit applications point to ongoing economic strength despite the high rates. I mean, firing people around Christmas is a d*** move. (Bloomberg has more on this)

Joke Of The Day

Momentum Investing: The fine art of buying high and selling low.

Value Investing: The art of buying low and selling lower.

Hot Headlines

The Globe | Pakistan fires retaliatory strike at Iran, stoking regional tension. It said the targets were bases used by the Baloch Liberation Front (BLF), a separatist group vying for the independence of the Baloch ethnic group in Pakistan, Iran and Afghanistan.

BBC | The unsuccessful American Peregrine moon mission ended with the craft destroyed over the Pacific Ocean. Had it been successful, it would have been the first US mission in 50 years and the first private venture to land on the moon.

Reuters | China widens South America trade highway with Silk Road mega port in Peru. The $3.5 billion deep water port aims to help provide Chinese access to the resource rich region.

Barron’s | EV sales plummeted in Europe in 2023 and hybrids fared even worse. Battery electric vehicles fell 25% from a year earlier to December, while plug-in hybrid sales fell 34%.

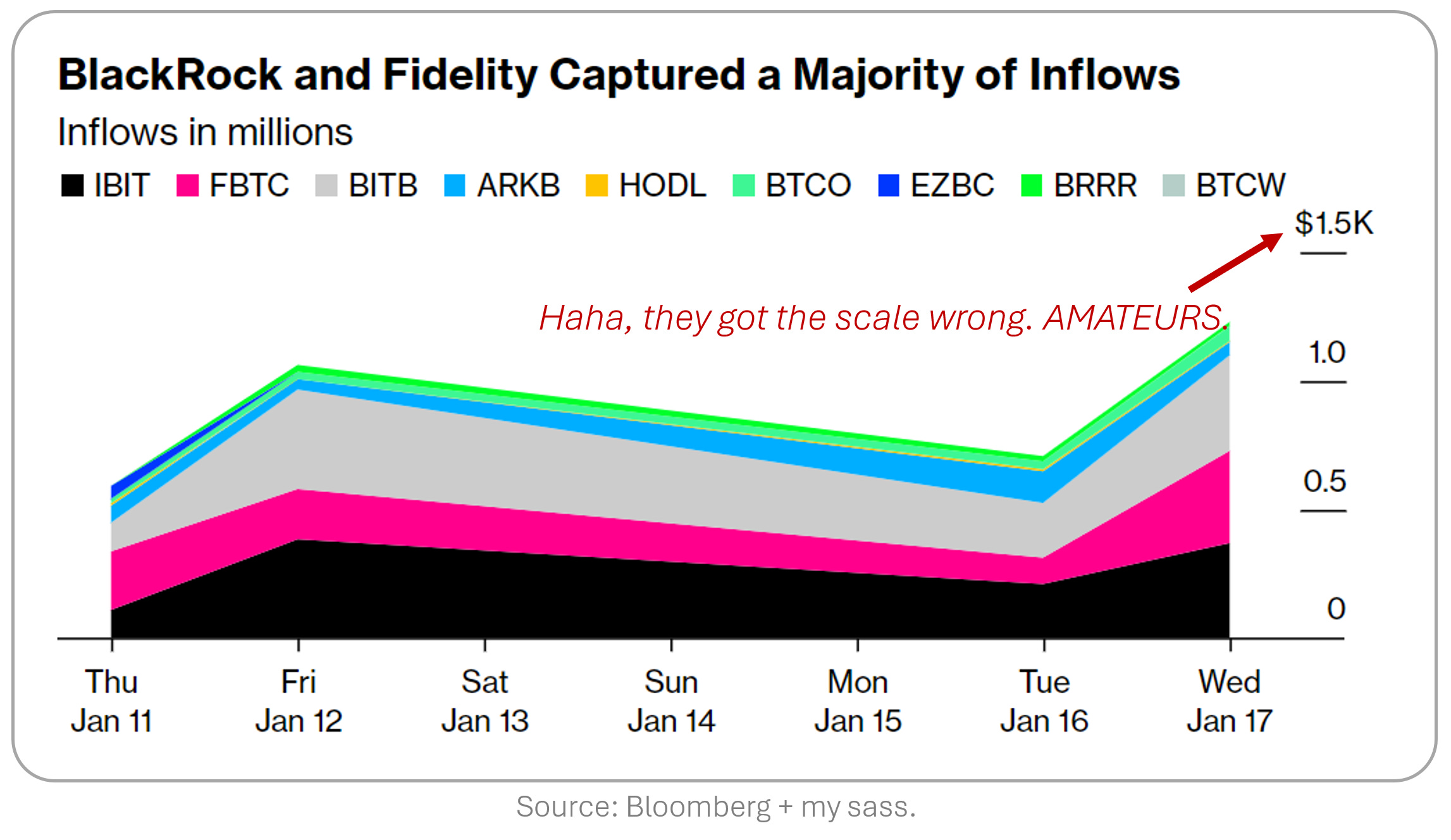

Bloomberg | BlackRock’s Bitcoin ETF first to break $1 billion in inflows. Fidelity nearby with $880 million. Shhhhh, no one mention that Bitcoin is down 11.3% since ETFs got approved.

Trivia

This week’s trivia is on corporate ‘firsts’.

What was the first computer to defeat a world chess champion?

A. Deep Thought

B. Deep Blue

C. AlphaZero

D. StockfishWhat was the first commercially successful video game?

A. Space Invaders

B. Pong

C. Pac-Man

D. TetrisWho was the first social media platform to reach 100 million users?

A. MySpace

B. Facebook

C. Twitter

D. LinkedIn

(answers at bottom)

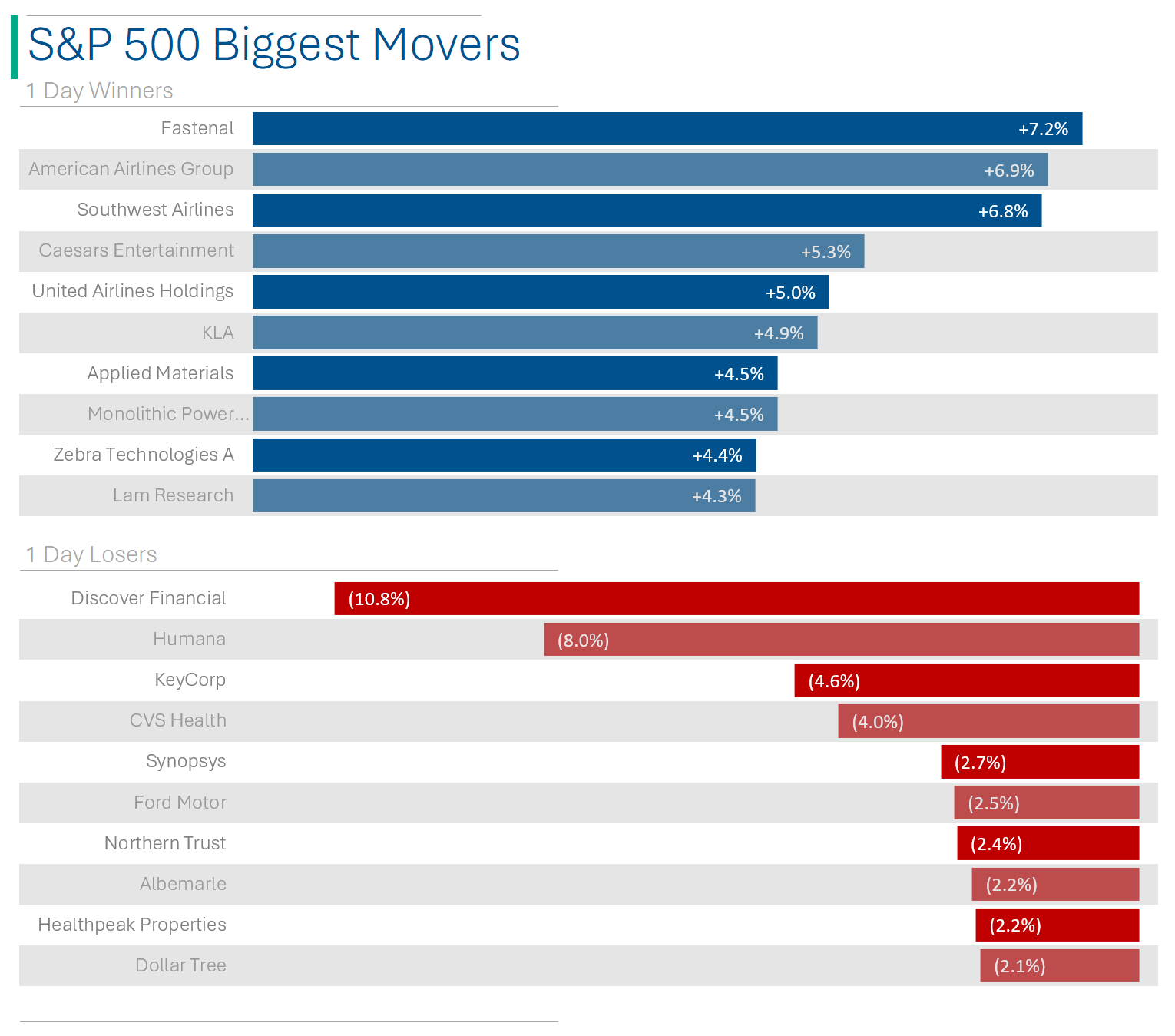

Market Movers

Winners!

M.D.C. Holdings (MDC) [+18.3%]: Sekisui House to acquire MDC for $63/share in a $4.9B deal, an 18% premium to yesterday's close. Expected to close in H1 of 2024.

Taiwan Semiconductor (TSM) [+9.8%]: Q4 results exceed expectations with strong 3 nanometer chip growth. Q1 revenue guidance surpasses consensus; 2024 revenue expected to increase in low-to-mid-20s%. AI seen as a major growth driver; some concerns about gross margins.

Hertz Global (HTZ) [+7.5%]: Morgan Stanley upgrades to overweight, citing better risk/reward balance, EV de-fleeting strategy, and potential to close gap with Avis.

Apple (AAPL) [+3.3%]: Upgraded to buy from neutral at BofA. AI and Vision Pro identified as key growth drivers for Hardware and Services.

Losers!

Discover Financial (DFS) [-10.8%]: Q4 EPS missed expectations despite revenue beat, impacted by higher provision expenses and operational costs. 2024 guidance weak, citing slowing loan growth and Net Charge-Offs (NCO).

Humana (HUM) [-8%]: Lowered FY23 EPS guidance by over 7.5% due to increased Medicare Advantage medical cost trends, particularly in inpatient utilization and non-inpatient trends in late 2022.

Birkenstock (BIRK) [-7.8%]: Q4 EPS slightly missed, while revenue and FY guidance exceeded expectations. Noted 16% quarterly revenue growth but warned of potential earnings pressure amid global expansion and higher operating expenses. haha, reminds me of the piece I wrote after their IPO: ‘Birken-flop’. I kill myself.

Spirit Airlines (SAVE) [-7.5%]: Downgraded to sell from neutral at Citi following federal judge blocking proposed merger with JBLU. Concerns raised about JBLU cutting losses and the uncertainty of new suitors for SAVE.

Market Update

Trivia Answers

B. Deep Blue was the first computer to beat a Chess World Champion. IBM’s Deep Thought lost to Champ Gary Kasparov in 1989 but the new and improved Deep Blue faced him again in May 1997, when it won the six-game rematch 3½–2½.

B. Pong was released in 1972 by Atari.

B. Facebook hit 100 million users in 2008.

Thank you for reading StreetSmarts. We’re just starting out so it would be great if you could share StreetSmarts with a friend that might be interested.