The S&P 500 Is Top Heavy, Consumer Spending Won't Quit, And Much More

StreetSmarts Morning Note

“Games are won by players who focus on the playing field –- not by those whose eyes are glued to the scoreboard.”

― Warren Buffett“The broker said the stock was "poised to move." Silly me, I thought he meant up.”

― Randy Thurman

Table of Contents

The S&P 500 Is Top Heavy: The Index Without The Top 10

Consumer Spending Stays Strong: But HOW?

Consumers Care About Prices Not Inflation

Apartment Building Starts Have Collapsed

‘Dangerous’ Underinvestment in Oil

Rivian Loses $33k On Every Vehicle

Powerball Payout Rises to +$1 billion

Trivia

Joke Of The Day

Main Indices

Global Market Indices

Global Commodity Prices

Global Exchange Rates

Interest Rates

The S&P 500 Is Top Heavy

The Index Without The Top 10

Only a few short days ago, the chatter about this ‘never ending market rally’ was getting pretty annoying (how times change quickly), and I decided to dig in a bit. As part of that, I made a graph showing the S&P 500 year-to-date returns for each sector. I then went on a bit of a spiel about Consumer Discretionary being overbought, especially given the fragile economy. It’s a pretty graph so I updated it and included it below.

Chatting with my wife last week over dinner later, I brought up the above and she countered to the effect, ‘well yeah, if you don’t count a handful of the biggest companies, the market hasn’t done that great.’ I hadn’t really thought about that before so I decided to prove her wrong look into it for myself.

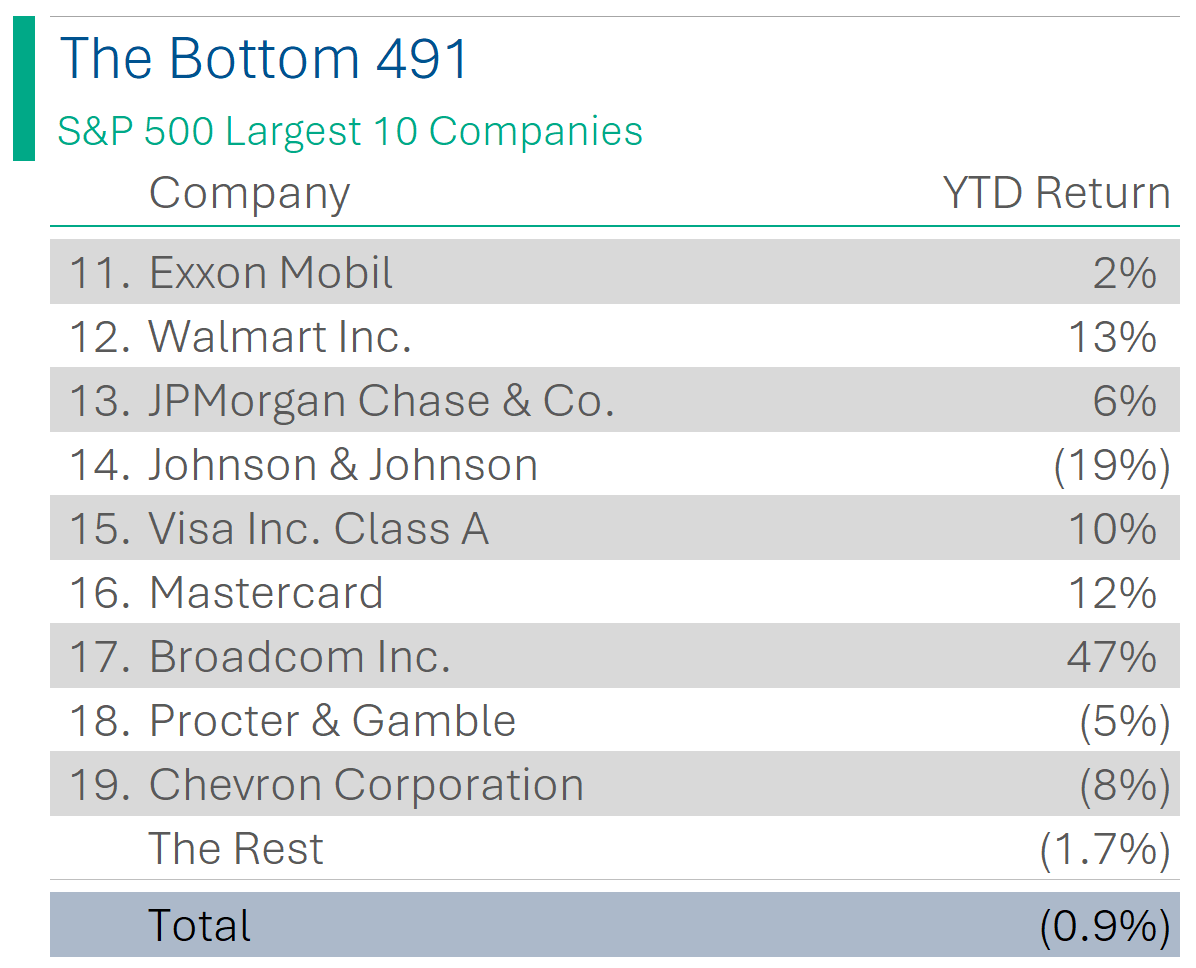

The S&P 500 consists of 503 share constituents (don’t ask). So what happens if you split it into two indices: the top 10 largest companies; and the 493 other ones? The results are pretty interesting. To start with, the S&P 500 is up 13.1% year-to-date. This is down from the 17.3% it was up as of September 14th, but still pretty solid for the year.

*** Before you ask, I removed Alphabet’s Class A shares for simplicity and the J&J spin-off, Kenvue, since it’s only been listed since May. That’s why it says 491 companies instead of 493***

Just looking at the above is pretty interesting: the largest 10 companies in the S&P 500 make up 33% of the index. The top 32 companies make up 50%. The S&P is really top heavy.

This is where it gets interesting: the top 10 companies in the S&P 500 were up a weighted average of 48% so far this year, while the rest are actually negative (-0.9%). Since the 1920s, the S&P 500 has averaged a return of just over 10% per year, so the S&P’s 12% year-to-date figure beats the historical average and is more than 100% driven by the top-10 companies.

And not to flog a dead horse here, but the top 10 companies added a total of $4.0 trillion dollars to the index this year. For context, the main Canadian index, the TSX Composite has a total market value of USD$2.3 trillion. The biggest 10 US companies added 1.7 ‘Canadas’ so far this year…

TLDR: My wife was right; I’m on kids’ lunch-making for the next week.

Consumer Spending Stays Strong

But HOW?

Americans spent 5.8% more in August than a year earlier, more than surpassing the sub-4% inflation rate. Delta Airlines reported a record second quarter; Ticketmaster saw sales up 18% in the first half of the year (thanks, Swifties!). For a number of economic reasons, people should be cooling things down for instance, pandemic savings are fully depleted for most people. Additionally, interest rates are up (that means a savings account does something for the first time in more than a decade). Regardless, people are still spending.

But why? There is increasing evidence of a new mindset among many consumers to enjoy life now (travel, spend freely, enjoy your money) with a renewed short-termism. Some of this can be attributed to moving on from the bomb shelter mentality of the COVID years. Some may also reflect sadder data, like people feeling a reduced desire to save for a house they increasingly feel they will never be able to afford. Or, that if economic times are destined to worsen, maybe it’s better to enjoy oneself now before the tough times.

Speed Round

Consumers Care About Prices, Not Inflation - WSJ did a nice piece looking at the impact that absolute price levels have on consumer confidence vs. what economists and the Fed care about, namely the inflation rate. Inflation recently ticked back up - mostly driven by oil - but it has come down dramatically from a peak of 9.1% in June of last year, to 3.7% at present. The consumer, the report alleges, remembers prices being lower and expects them to decline to pre-COVID levels. The fact that the majority of prices are still materially elevated and show little likelihood of ever depreciating is hurting consumer confidence. Explaining that the aim of policy makers is for wages to rise to face these new price levels, as opposed to trying to trigger deflation (which can cause a dangerous spiral) is of little consolation. Sorry folks, the only way we’re seeing $1.60 Big Macs again means something has gone terribly, terribly wrong with the economy. WSJ Article.

Apartment Building Starts Has Collapsed - Construction data, such as housing and building starts, are excellent leading indicators for the health of an economy. Building starts for apartments in the US have fallen to a seasonally adjusted rate of 334k units in August, a 41% decline from a year earlier. Real estate data firm Bright MLS says the only time a decline like this has happened before was in the fall-out from the subprime crisis. Part of this can be attributed to record construction in recent years (more rental buildings are being completed this year than at any other time in the US since the 1980s) and partly due to the burden interest rates are placing on developers. WSJ cited one developer who said he has seen his borrowing costs increase from 4% to 8%. The impact of all of this is starting to show its face in vacancy rates which are back above pre-pandemic levels and don’t appear to be slowing. WSJ Article.

‘Dangerous’ Underinvestment in Oil - Haitham Al Ghais, OPEC’s secretary-general, claims the world needs to be investing a lot more in oil - $12 trillion to be exact (by 2045) - in order prevent a dangerous spike in oil. These people. No one tell him we’re trying to do the opposite right now. CNN Article.

Rivian Loses $33k On Every Vehicle - Rivian - the self-proclaimed ‘Tesla of Trucks’ - loses nearly the value of a base F-150 on nearly every vehicle it sells. Its 2021 IPO was one of the largest in years; raising $12 billion to make the cash pile $18 billion…but they have burnt through half of it in two short years. WSJ Article.

Powerball Payout Rises to +$1 billion - Not business related, but still crazy. No one claimed the prize on Friday, so the new prize has been upped to an estimated $1.04 billion making it one of the 10 highest in history. Morningstar Article.

Grab Bag

Trivia:

What was the first company in the world to reach a market capitalization of $1 billion?

U.S. Steel

General Electric

Standard Oil

J.P. Morgan & Co

What company was a member of the Dow Jones Industrial Average for the longest amount of time?

General Motors

Coca-Cola

General Electric

IBM

(answers at bottom)

Joke Of The Day:

Market Update

Main Indices

Global Market Indices

Global Market Indices

Global Commodity Prices

Global Exchange Rates

Interest Rates

Trivia Answers:

U.S. Steel. After J.P. Morgan (the guy, not the bank) arranged to buy Carnegie Steel to create the world’s largest steel company and merge it with his steel operations, he needed to raise significant capital to streamline the operations. To do this Morgan issued $303 in mortgage bonds, $510 million in Common Stock, and $508 million - thus creating the first billion dollar company!

General Electric. The company was a member of the Dow from 1896 to 2018. Just one more thing to be annoyed with about the tenure of Jeff Immelt who left the company a shadow of itself, while he was busy flying around in a private jet, followed by another private jet (just in case the first one needed repairs). What a clown.

Thank you for reading StreetSmarts. We’re just starting out so it would be great if you could Share and Subscribe!