🔬Revenge of the Laggards

Plus: that Rate Cut feelin'; QXO's divebomb; and much more!

"Wide diversification is only required when investors do not understand what they are doing."

- Warren Buffett

“I'm tired of hearing about money, money, money, money, money. I just want to play the game, drink Pepsi, and wear Reebok.”

- Shaquille O'Neal

Another soft day for the big US markets with the S&P 500 -0.5% and Nasdaq -1.3%. Small-Cap still doing work with the Russell 2000 +0.4%.

7 of 11 sectors closed higher but when Tech (-2.2%) has a day like that, it all ends in the red. Energy (+1.5%) and Financials (+1.2%) were tops again.

July Consumer Confidence came in at 100.3 vs. estimates for 99.5 but June’s was revised down (97.8 from 100.4), so a bit mixed.

Germany unexpectedly posted Q2 GDP down 0.1% despite broader Eurozone coming in +0.3%.

Notable companies:

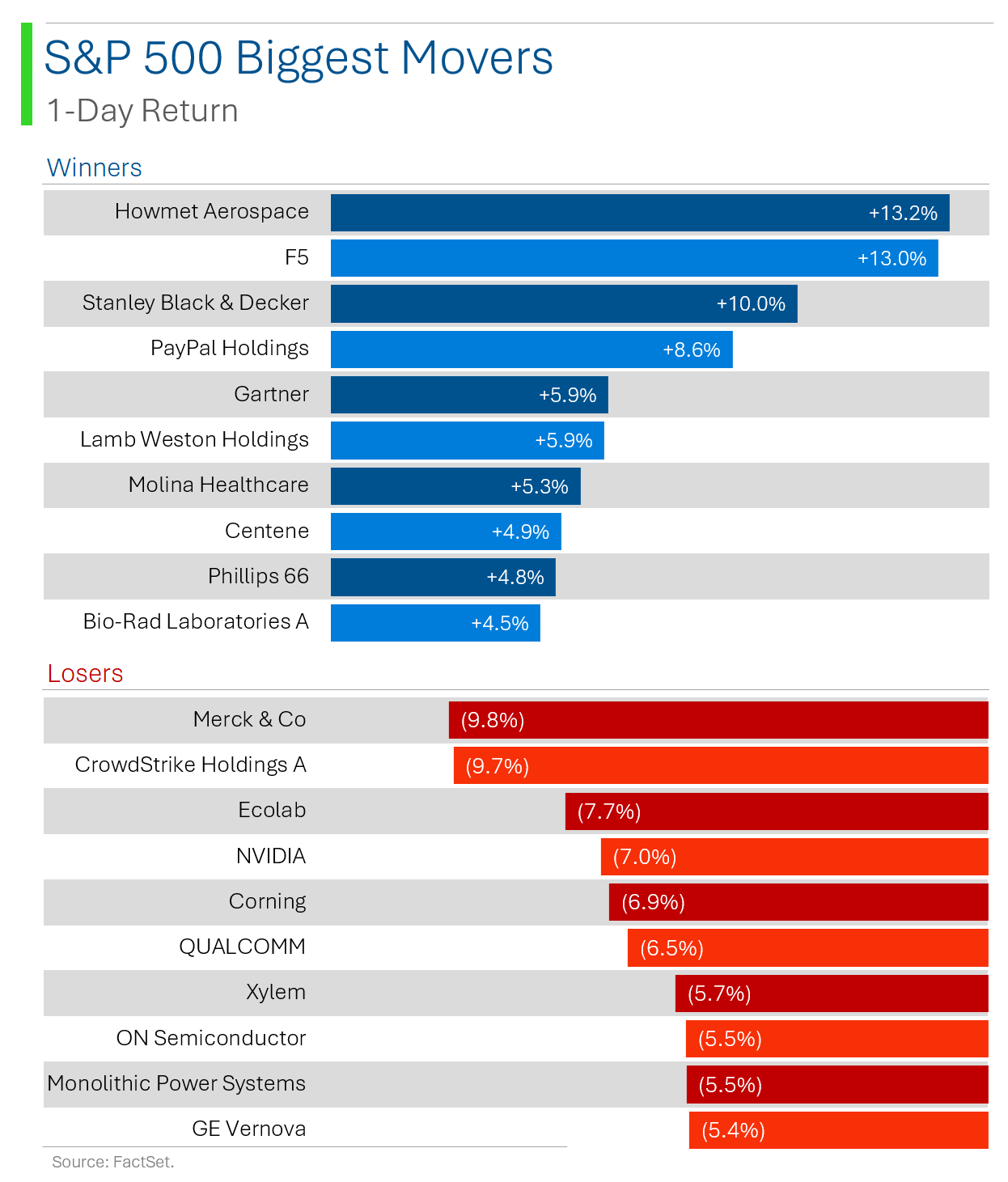

JetBlue Airways (JBLU) [+12.3%] Q2 EPS and revenue beat, Q3 revenue guidance below consensus but FY24 revenue growth guidance raised. Focus on restoring balance sheet health and positive FCF.

Merck (MRK) [-9.8%] Q2 earnings and revenue beat. Keytruda ahead of consensus, Gardasil light due to China shipment timing. Slight raise to FY revenue guide.

CrowdStrike (CRWD) [-9.7%] CNBC reported Delta seeking damages from recent outages. Analysts estimate Delta's operational damages at $350-500M, excluding reputational damages.

Procter & Gamble (PG) [-4.8%] FQ4 core EPS better, revenue and OM missed. Organic growth light across all segments. FY25 guidance bookends consensus, forecasts unfavorable commodity costs and FX.

More below in ‘Market Movers’.

Street Stories

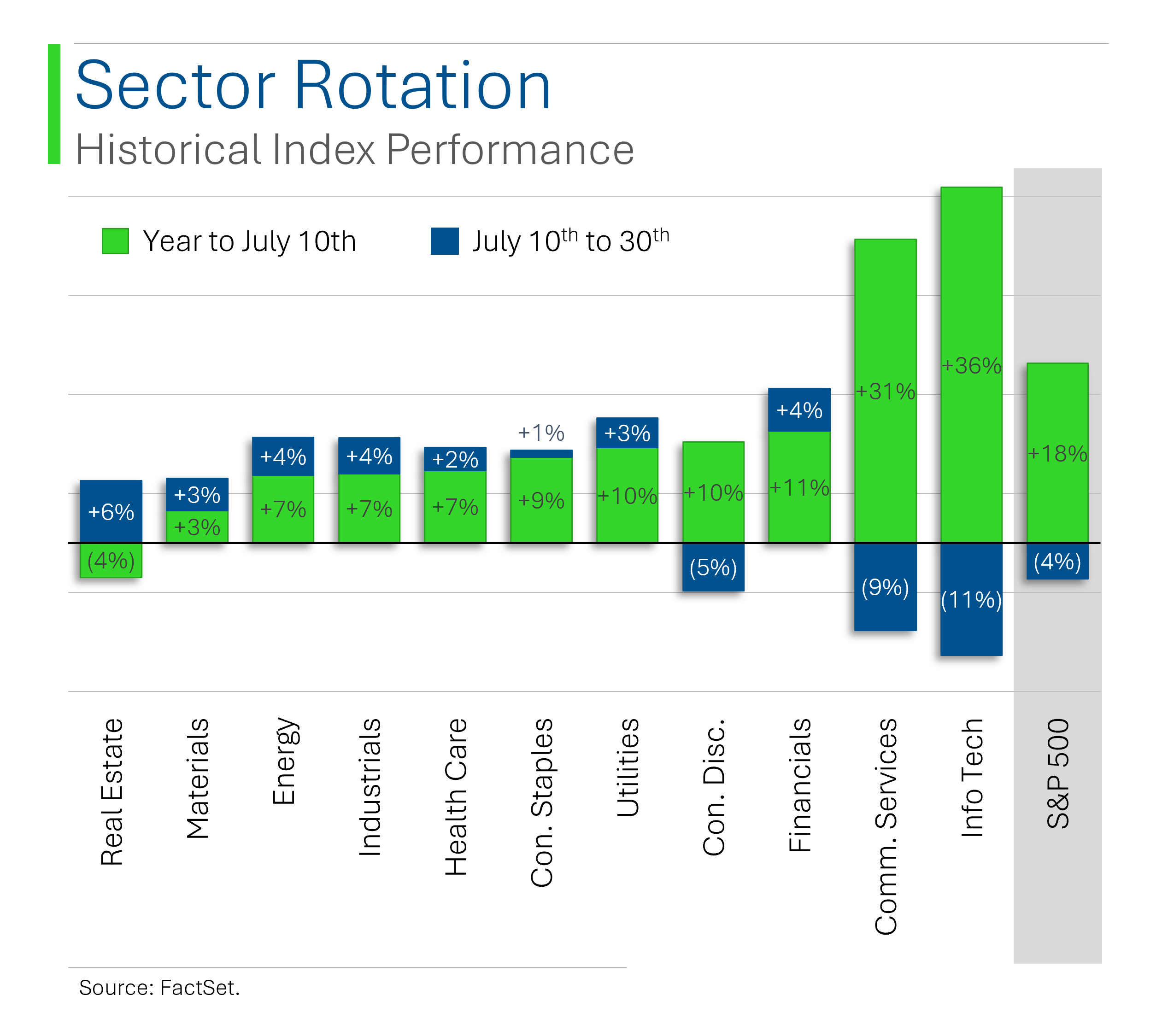

Revenge of the Laggards

There has been a lot written - including from moi - about this rotation hammering the winners and passing it on to lagging Small-Cap. This has notably come from Tech and the techy bits of Communication Services (Meta, Alphabet, Netflix) but it’s not so clear cut; even from a sector perspective.

To start, yes, the sectors that have done the worst this year (Real Estate, Materials, Energy and Industrials) have been some of the best performers since the rotation kicked-off circa July 10th.

Winners into losers. Check.

But even within certain sectors, we are seeing a massive shift from the winners into the losers laggards.

Take Communication Services for example: Nearly all the big winners of the year have seen an exodus (save for Fox, but that’s probably more to do with the election ramp-up), but the ‘value’ buys are all up quite significantly in the last 3 weeks.

Only Paramount Global has continued to lag - and, here again, that has more to do with the sketchy merger with Skydance.

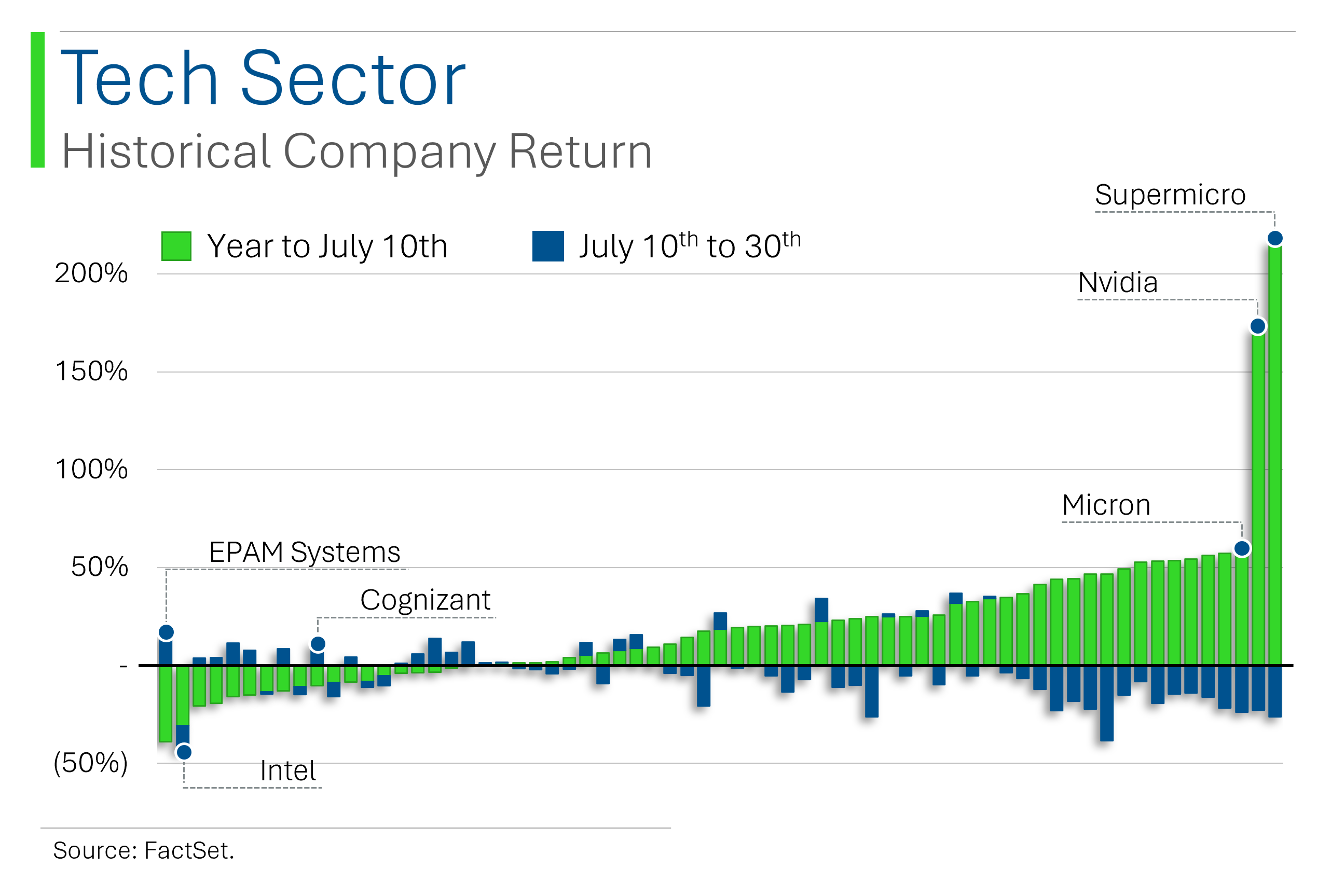

Even within Tech we see the ‘value’ - ie: laggards - catching a bid recently. Only Intel really stands out as continuing to suck (even value rotations can’t help if you’re a melting ice cube).

(For a bit more background check out my two-parter, Intel’s Lost Chip Crown (Part I) (Part II), which explains their downfall in pretty charts.)

Don’t worry, I won’t do this for all 11 sectors, but I do want to highlight Healthcare and Industrials for different reasons.

See, Health Care is arguably the biggest winner of this rotation - save for a few exceptions (Edwards, a medical equipment company, and Dexcom, a diabetes monitoring company, both blew up after weak earnings and guidance).

The outperformance of Health Care is broadly driven by it being considered a ‘Defensive’ sector, like Utilities and Consumer Staples.

Industrials, on the other hand, is more of a cyclical sector.

It’s a bit unique that both defensive and cyclicals are working hand-in-hand here. Investors seem to be betting that the economy is on a sound enough footing that Industrials will work, but also hedging a bit with the positioning into defensives (Healthcare) as well.

To finally tie everything together from an index perspective, the rotation is impacting lots of different sectors and classifications. In many cases, the biggest winners of the year are having a bad time, while the laggards are (finally) playing a bit of catch-up.

Within the S&P 500, the companies that were up +40% prior to the July 10th transition are now down an average of -15.7%. The stocks that were down between 0% to -10% are up +6.5% since July 10th.

Mr. Market has been pulled over by the Fun Police.

Rate Cut Ready

The Federal Reserve’s July Federal Open Market Committee (FOMC) meeting concludes today with Jerome Powell (J-Pow to his friends) set to announce the latest round of interest rate decisions for the good ole U-S-of-A.

Odds of cut today sit at just ~5.2%, so don’t expect any fireworks.

What is worth noting is that the next meeting, set for September, is pretty much a given at this point. Interest rate futures (which are never ever wrong) are currently pricing the odds of at least one 25 basis point cut at that meeting at 100% - up from just a 47% likelihood at the end of May.

QXO(hhhhh f***)

The blank cheque company QXO that counts Jared Kushner as a board member, traded at a valuation as high as $157 billion earlier this year but that is very much no longer the case.

After filing a private placement on Monday evening, the company announced plans to take the current number of shares from 665k to roughly 400 million.

Bonfires ensued.

Joke Of The Day

I told my female colleague that she drew her eyebrows too high. She seemed surprised.

Hot Headlines

Reuters / Meta agrees to pay $1.4 billion to settle Texas facial recognition data lawsuit. The settlement relates to Meta collecting biometric data for millions of Texans and is reportedly the largest single settlement with a single state in history.

CNBC / CrowdStrike takes another 9.7% header on news that Delta Air Lines is planning to sue over damages from cyber shutdown. The airline is currently dealing with 176k refund or reimbursement requests after +7k flights were cancelled.

Yahoo Finance / Oil & Gas mergers continued at a furious pace in Q2. Enverus research points to 18 tie-ups in the quarter totaling $30.3 billion, even as regulators seek to pump the brakes on further consolidation.

Bloomberg / Hedge Fund weenie Bill Ackman’s planned $25 billion takes another step backwards. The August 5th IPO of Pershing Square is now expected to only target $2 billion.

Reuters / OPEC+ likely to stick to output policy at Aug 1 meeting. The group currently has cuts of ~5.9 million barrels per day (5.7% of global demand) in place but insiders report that further cuts aren’t going to take place despite recent pull back in oil prices.

Trivia

Today’s trivia is on the legendary investor Ben Graham.

Benjamin Graham wrote a famous book on investing, which is this?

A) The Wealth of Nations

B) The Intelligent Investor

C) Security Analysis

D) Common Stocks and Uncommon ProfitsWhich future billionaire was a student of Benjamin Graham at Columbia University?

A) Bill Gates

B) Stan Druckenmiller

C) Warren Buffett

D) George SorosWhich of the following concepts is NOT associated with Benjamin Graham’s investment philosophy?

A) Margin of Safety

B) Efficient Market Hypothesis

C) Mr. Market

D) DiversificationGraham was a pioneer of a particular type of analysis for evaluating stocks. What is it called?

A) Fundamental analysis

B) Technical analysis

C) Sentiment analysis

D) Predictive analysis

(answers at bottom)

Market Movers

Winners!

Varonis Systems (VRNS) [+14.6%] Q2 results beat, Q3 guidance ahead, and FY outlook raised. Highlights: new log strength, MDDR adoption tailwind, more recurring revenue, shorter sales cycles, AI opportunities flagged, upgraded at Baird.

Howmet Aerospace (HWM) [+13.2%] Q2 EPS and revenue beat, Q3 EPS and revenue guidance ahead, FY24 earnings and revenue guidance raised, $2B share buybacks increase. Strong commercial aerospace outlook with travel demand and aging aircraft fleet.

F5, Inc. (FFIV) [+13%] FQ3 earnings, revenue, and margins beat. Strong software renewals, solid demand with improving pipeline and close rates, raised FY guidance, better than feared report.

JetBlue Airways (JBLU) [+12.3%] Q2 EPS and revenue beat, Q3 revenue guidance below consensus but FY24 revenue growth guidance raised. Focus on restoring balance sheet health and positive FCF.

Stanley Black & Decker (SWK) [+10%] Q2 EPS beat on in-line sales. Margin boost from lower inventory destocking costs, shipping costs, and supply chain transformation. Strength in DEWALT, outdoor, and aerospace fasteners, raised FY EPS and FCF guidance.

PayPal (PYPL) [+8.6%] Q2 earnings and revenue beat. Take rate and transaction margin above consensus, best transaction margin dollar growth since 2021, raised FY guidance for EPS, transaction margin, FCF, and buybacks.

Phillips 66 (PSX) [+4.8%] Q2 earnings beat with strong results from Refining and Midstream. Positive on buybacks and smaller-than-expected renewables loss.

American Tower (AMT) [+3.8%] Q2 earnings and revenue beat, FY24 adj EBITDA, AFFO, and total property revenues raised. Positive collection trends in India, CoreSite’s second highest quarter of signed new business on record.

Losers!

Merck (MRK) [-9.8%] Q2 earnings and revenue beat. Keytruda ahead of consensus, Gardasil light due to China shipment timing. Slight raise to FY revenue guide, EPS guide trimmed on acquisition factors.

CrowdStrike (CRWD) [-9.7%] CNBC reported Delta seeking damages from recent outages. Analysts estimate Delta's operational damages at $350-500M, excluding reputational damages.

Lattice Semiconductor (LSCC) [-9.4%] Q2 results missed, Q3 guidance below. Continued headwinds from inventory destocking, particularly in Industrial and Automotive. Noted some improvement in booking trends.

Ecolab (ECL) [-7.7%] Q2 EPS in line, Q3 EPS guidance also in line. Sale of global surgical solutions business to negatively impact 2H24 by ~$0.08. Reported slowdown in QSR activity by major customer.

Corning (GLW) [-6.9%] Q2 EPS ahead of preannounce, revenue in line. Q3 EPS and revenue midpoints slightly below Street. Gen AI tailwind to Optical Communications offset by trucking segment.

Procter & Gamble (PG) [-4.8%] FQ4 core EPS better, revenue and OM missed. Organic growth light across all segments. Increased promotions for Fabric/Home Care, share losses in Baby/Family. FY25 guidance bookends consensus, forecasts unfavorable commodity costs and FX.

Archer-Daniels-Midland (ADM) [-1.3%] Q2 EPS and revenue missed, FY24 guidance reaffirmed. Operating profits for Ag services & oilseeds down steeply y/y. Results driven by slower farmer selling in South America (anticipated) and increased supply from Brazil and Argentina. Carb solutions beat.

Market Update

Trivia Answers

B) Graham wrote The Intelligent Investor.

C) Warren Buffett was a student and mentee of Graham.

B) The Efficient Market Hypothesis isn’t something Graham is known for. That was Eugene Fama in 1970.

A) Graham literally wrote the book on Fundamental analysis.

Thank you for reading StreetSmarts. We’re just starting out so it would be great if you could share StreetSmarts with a friend that might be interested.